Introduction

Non-metropolitan towns and cities are vital to our nation’s social and economic fabric. They anchor rural economies, act as gateways to the natural environment, and sustain a unique way of life.

Despite their differing regional and economic contexts, non-metropolitan areas face shared challenges: rising housing costs, struggling high streets, and pressures on funding and governance, all of which threaten their long-term sustainability.

Housing-led regeneration has emerged as a key strategy to help address these challenges. By leveraging housing development as a driver of investment and renewal, local leaders are meeting immediate housing needs while delivering broader economic and social benefits. Working with central government and private sector partners, they are pioneering new approaches to overcome viability barriers and attract investment.

This report explores the transformative impact of housing-led regeneration through nine case studies, supported by analysis of housing delivery in non-metropolitan settlements across England. It highlights practical approaches to overcoming delivery barriers and evidences the important contribution these places make to national housing delivery.

With English devolution promising to empower regional leaders, alongside reform of the planning system, this report reinforces the importance of keeping non-metropolitan towns and cities firmly in focus, ensuring their potential is fully realised and enhanced in the years ahead.

Defining non-metropolitan areas

This report defines non-metropolitan areas as the rural and sub-urban towns and cities located outside the main city regions of England. These areas are identified by combining two key Office for National Statistics (ONS) classifications:

Towns and Cities that are classed as ‘Small’, ‘Medium’ or ‘Large’ ‘Built Up Areas’ (BUAs), as defined by ONS, that are situated within local authorities identified as ‘largely rural’, ‘mainly rural’ or ‘urban with significant rural’ as per the ONS Rural Urban Classification, excluding Local Authorities within established City Regions.

By focusing on these discrete settlements rather than broader rural districts, the analysis provides a clearer view of distinct housing trends surrounding non-metropolitan town centres.

Using this definition, we identify 226 non-metropolitan settlements in England. On average, each settlement contains approximately 15,300 homes and 33,600 residents. A regional breakdown of non-metropolitan areas is outlined below, with a map provided on Page 20.

Methodology

This report combines a review of regeneration and housing literature, data analysis, and case study interviews to understand housing delivery and regeneration in non-metropolitan settlements.

Literature Review

A review has been conducted to identify recent findings in relation to new housing in non-metropolitan settlements and town centres in academic, government and industry publications. This has been complemented by an assessment of recent national government funding programmes for the regeneration of towns, such as the Towns Fund and Levelling Up Fund.

The research identified primary barriers to delivering housing in town centres and a set of best-practice approaches to delivery, which have been set out in this report.

Data analysis

Having defined non-metropolitan settlements, Prior + Partners created a data tool to investigate and analyse housing and socio-economic data in non-metropolitan settlements as well as aid the process of selecting appropriate case studies. The tool spatialised all non-metropolitan settlements within our definition and integrated multiple quantitative datasets on socio- economic context and housing supply, delivery and town centre performance.

Key characteristics and trends in housing in non-metropolitan settlements have also been analysed and summarised in the report. The housing analysis was used to identify towns that were relevant to the study and to ensure a representative sample of areas. For example, a spatial representation of change in housing stock at the small area level helped identify towns where housing delivery has taken place in town centres, rather than on the edge of towns.

Case study interviews

A shortlisting process was undertaken to select the case studies.

A longlist of 20 non-metropolitan settlements was produced in the first instance, which was built up from the LGA, Prior + Partners, and Newsteer teams’ combined knowledge, qualitative research, as well as systematic research of quantitative and spatial data through our analytical data tool.

Summary profiles of the 20 non-metropolitan settlements selected were produced which describe the approach taken to housing delivery and regeneration in each area, and the key issues and lessons to be explored. These were shared with the LGA’s People and Places Board for review. A representative sample of nine areas considered most relevant to the study were researched further through in-depth interviews with the respective councils.

The project team translated findings from the above into lessons and recommendations aimed at supporting councils.

Literature review

Extensive analysis and debate on town centre regeneration and housing delivery have taken place across academia, government, and industry. This review considers recent writing on several relevant themes, including different strategies for regenerating declining town centres, lessons from mixing residential uses with other uses in town centres and the feasibility of delivering different town centre housing typologies, including above-retail conversions and large-scale brownfield projects.

An overview of recent regeneration funding programmes, such as the Towns Fund and Levelling Up Fund is provided, summarising the support for housing development in non-metropolitan settlements in national government policy.

Findings have been synthesised into key lessons, including a set of primary barriers to housing in non-metropolitan settlements and corresponding best-practice approaches to delivery which have informed case study interviews.

Literature review and policy context

A review of recent literature from academic, government, and policy sources highlights several key themes influencing town centre housing development. A summary of the literature is provided below.

The changing role of town centres

Recent research on town economies and regeneration has identified the need for different growth models for town centres going forward, with greater mixing of uses and residential densification recurring themes. In particular, it is emphasised that town centres should push for more experiential offerings (leisure, communal dining), intergenerational living and more specialised retail. Reports emphasise that many towns can no longer rely on retail as a means of ensuring vitality, with greater residential development often cited as a suitable tool to promote renewal. Shifting commuting patterns in the wake of COVID-19 are also widely reported as a significant disruptor to traditional town centre models, with large-scale office development no longer a reliable means of ensuring vitality for many towns.

Town centre housing types

There are various established approaches and typologies of town centre housing development identified in the literature. Typologies include:

- conversion of larger retail units

- conversion of small ancillary or storage spaces above retail units on high street

- redevelopment of larger council-owned assets to deliver housing

- large-scale residential development on fringe city centre brownfield sites, such as next to railway stations.

The literature identifies the need for thoroughly different public sector interventions depending on housing typology. For instance, the delivery of high-street residential requires careful consideration of factors such as the age and condition of buildings, compliance with building regulations, and the potential impact on town centre retail activity.

Housing delivery barriers

Town centres experience many of the same structural barriers to housing deliver as much of the UK. Specific obstacles to housing delivery in non-metropolitan town centres identified in the literature include:

- the difficulty of assembling sites and attracting funding

- minimising costs when developing units on town centre high streets

- the current complexity of Compulsory Purchase Order (CPO) legislation

- the lack of clear guidance and support for town centre residential development in local plans and stringent parking requirements on constrained sites.

To overcome these barriers, many of the reports suggest reform to the VAT regimen (which is currently charged when converting high street units to residential), CPO legislation, and more dedicated policy on town centre housing in local plans. Similarly joint ventures between local authorities and specialised town centre developers are seen as the optimal delivery vehicle for realising this form of development.

Recent national government funding programmes

As part of literature review, we looked at recent government funding programmes relevant to non-metropolitan areas. The past five years has seen a wave of national government funding programmes with a focus on stimulating town centre and high street regeneration outside of England’s major cities. A total of £10.5bn has been allocated across the UK Shared Prosperity Fund, the Towns Fund, and the Levelling Up Fund (LUF), alongside other initiatives like Town Deals and the Brownfield Land Release Fund. This has supported a broad national programme of town centre regeneration, land remediation, and cultural, transport, and infrastructure projects.

Analysis of successful Town Deals and LUF projects shows that a significant proportion feature a town centre housing component. Towns Fund projects include the conversion of town centre retail to residential, as with the plans to convert the vacant M&S and BHS units to housing in Northampton. In Blyth, £18m out of £21m in funding is going towards the refurbishment of rundown existing housing units, with Mansfield also using a tranche of funding to adapt town centre housing estates. Hastings and Dewsbury will see the delivery of a small number of town centre homes in historic conversions, while Towns Fund grants will be used to finance largescale transport-oriented brownfield development in Worcester.

Numerous projects identified in the case studies in chapter “04 Case Studies” received government funding including the Levelling Up Fund, the Towns Fund, and the Brownfield Land Release Fund. Selected examples of projects with a housing component funded via the Towns Fund are set out in the map.

Findings from the literature review

Following review of the literature, a number of barriers and challenges to delivering housing in town centres and on high streets have been identified. Likewise, case studies identified in the literature have provided an idea of successful approaches to delivering housing in town centres.

Barriers to delivering town centre housing in non-metropolitan areas

- Complex land ownership

Town centres tend to have smaller plots which are often spread across a greater number of individual owners. This makes assembly of smaller plots into a single parcel a complicated and often lengthy process, which requires negotiation with multiple stakeholders and may require use of Compulsory Purchase powers.

- High build costs

Town centres often have older building stock, which can make conversion to residential units more expensive than for standard units[1]. Making units compliant with Building Regulations or decarbonisation or energy efficiency targets, or access requirements incur additional costs.

- Unclear or out-of-date planning policies:

The lack of precise and affirmative policy and design guidance in Local Plans supporting town centre housing often deters investors. Parking or Section 106 requirements for town centre sites are also often not aligned with the space or financial fundamentals of the site[2] .

- Financial risk for councils

Significant upfront investment requirements, need for specialist delivery support and long-term commitment to delivery introduce significant risk and uncertainty for council-led schemes.

- Compulsory purchase legislation

Inconsistent Compulsory Purchase Order processes heighten litigation risks, constrain councils’ ability to drive housing delivery and delay redevelopment.

- Public and political opposition

Local opposition has often hindered the delivery of town centre housing. In some cases, local residents who fear losing major retailers may also oppose developments that could support a sustainable local economy. In this context, political leadership can be decisive in ensuring that well-designed developments receive support through the planning process.

Best practice for delivering town centre housing in non-metropolitan areas

- Streamlined governance

A strong and integrated vision for town centres relies on targeted and dedicated governance. This might mean assembling a dedicated town centre team within the council or empowering the local Business Improvement District to deliver a program of improvements.

- A clear investment narrative

Ensuring that town centres sites are proactively marketed, simplified and improved so that they form a compelling investment prospect which can be taken to the market. This has been done successfully by using public grant to enable land remediation or land assembly.

- Affirmative planning policy

Providing explicit planning policy and guidance on town centre housing can help de-risk private development by providing developers with greater certainty. For example, producing a dedicated Supplementary Planning Document for town centres with explicit guidance on housing delivery and design has proven helpful. Likewise, specific Design Codes for town centres, can help minimise developer risks relating to the quality of design.

- Public / private joint ventures

Where large-scale housing has been successfully delivered in town centres, this has often been as a result of extensive collaboration between the public and private sectors, with councils consolidating sites and the private sector providing necessary capital and expertise.

- Different housing types and tenures

Offering different housing types (such as apartments and townhouses) and tenures (student housing, purpose-built housing for the elderly) enables a more resilient town centre offer and encourages mixing of different groups.

[1]Heritage Works for Housing, 2024, Historic England

[2]A New Urban Settlement: Fixing the Affordable Housing Crisis in Rural England, 2018, Institute for Public Policy Research

Analysis of housing in non-metropolitan settlements

Introduction

England’s urban fabric extends far beyond its biggest cities. This analysis examines the characteristics of housing in the 226 identified non-metropolitan settlements, highlighting their unique attributes and contributions to national housing delivery. These areas are shown on the map below.

It explores how these areas contribute to housing growth while driving regeneration and supporting broader national priorities. By identifying shared traits and regional variations, the analysis uncovers patterns in housing delivery, considering factors such as affordability and local economic performance.

Housing characteristics in non-metropolitan settlements

One in seven homes in England is in a non-metropolitan settlement

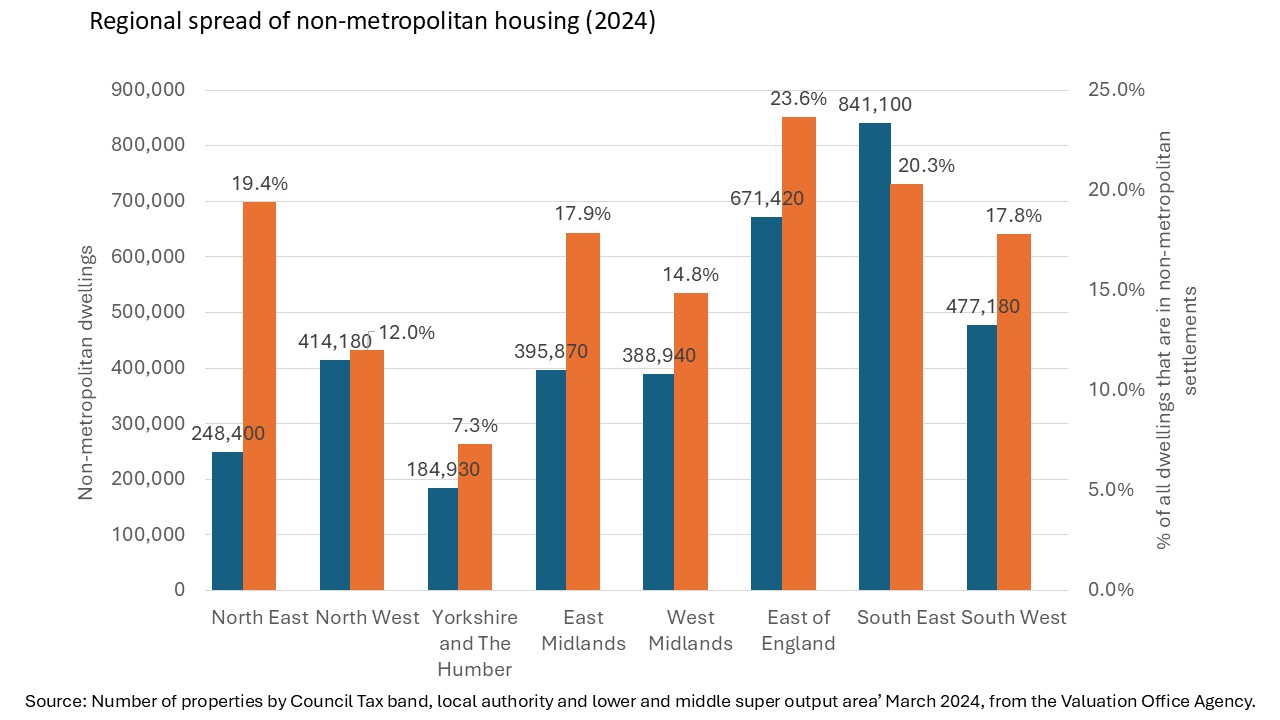

Non-metropolitan settlements are home to almost 7.6m residents and 3.6m homes, equal to 14.2 per cent of all housing in England (25.6m).

The distribution of these settlements varies markedly by region, reflecting differences in rurality and urbanisation. In the East of England, non-metropolitan settlements provide 23.6 per cent of all housing stock, compared to only 7.3 per cent in Yorkshire and the Humber.

The majority of non-metropolitan housing is concentrated in three regions: the South East (23.2 per cent), East of England (18.5 per cent), and South West (13.2 per cent). Settlements in these regions tend to be smaller but more numerous, whereas the Midlands and North have fewer, more concentrated settlements.

This fundamental difference in settlement pattern accounts for the higher proportion of non-metropolitan housing stock in the South compared to other regions.

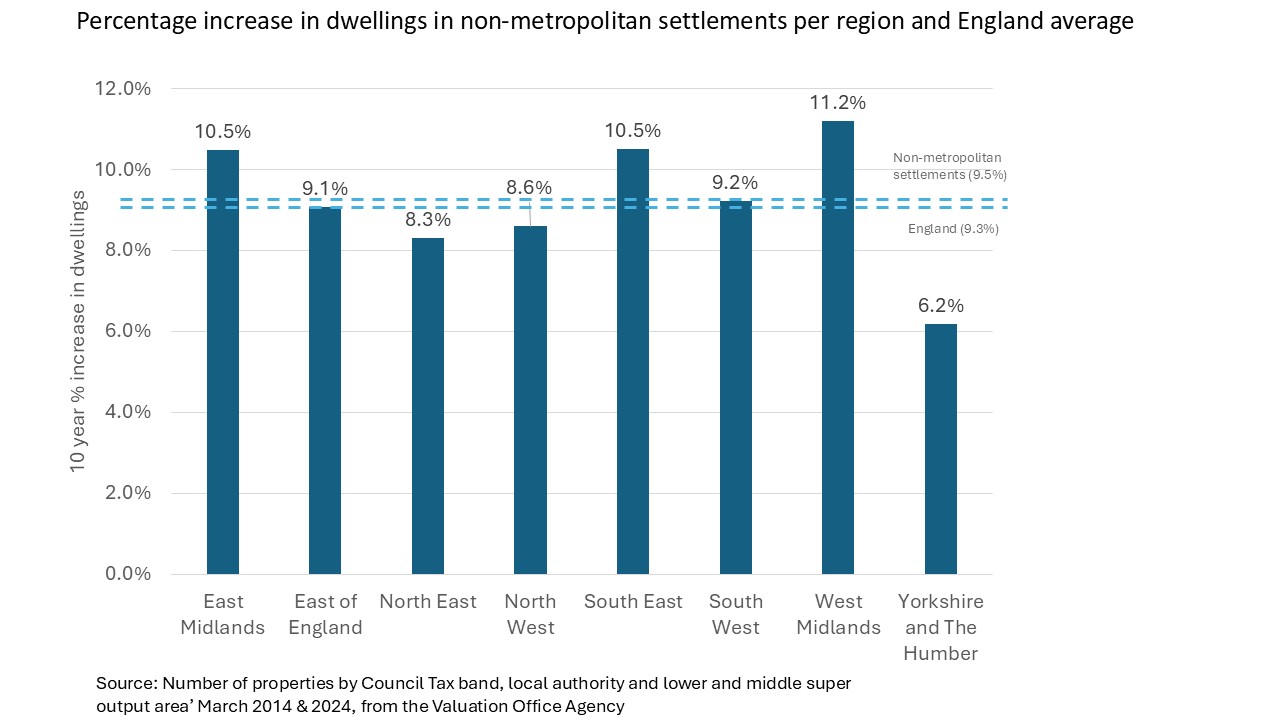

Non-metropolitan settlements have added 315,500 homes in the past decade, more than London.

Between 2014 and 2024, non-metropolitan settlements delivered 315,500 new homes, representing 14.5 per cent of England’s total new housing and surpassing the 301,700 homes delivered in Greater London.

The rate of increase in non-metropolitan settlements of 9.5 per cent is on par with the rate of increase of 9.3 per cent across England, though regional differences emerge in both volume and rate of delivery.

Leading regions also dominated supply, with the South West (79,900 added), East (55,900), and South East (40,290) contributing 56 per cent of national non-metropolitan housing growth.

The West and East Midlands delivered fewer homes yet achieved strong growth rates of 11.2 per cent and 10.5 per cent, respectively, surpassing the national average.

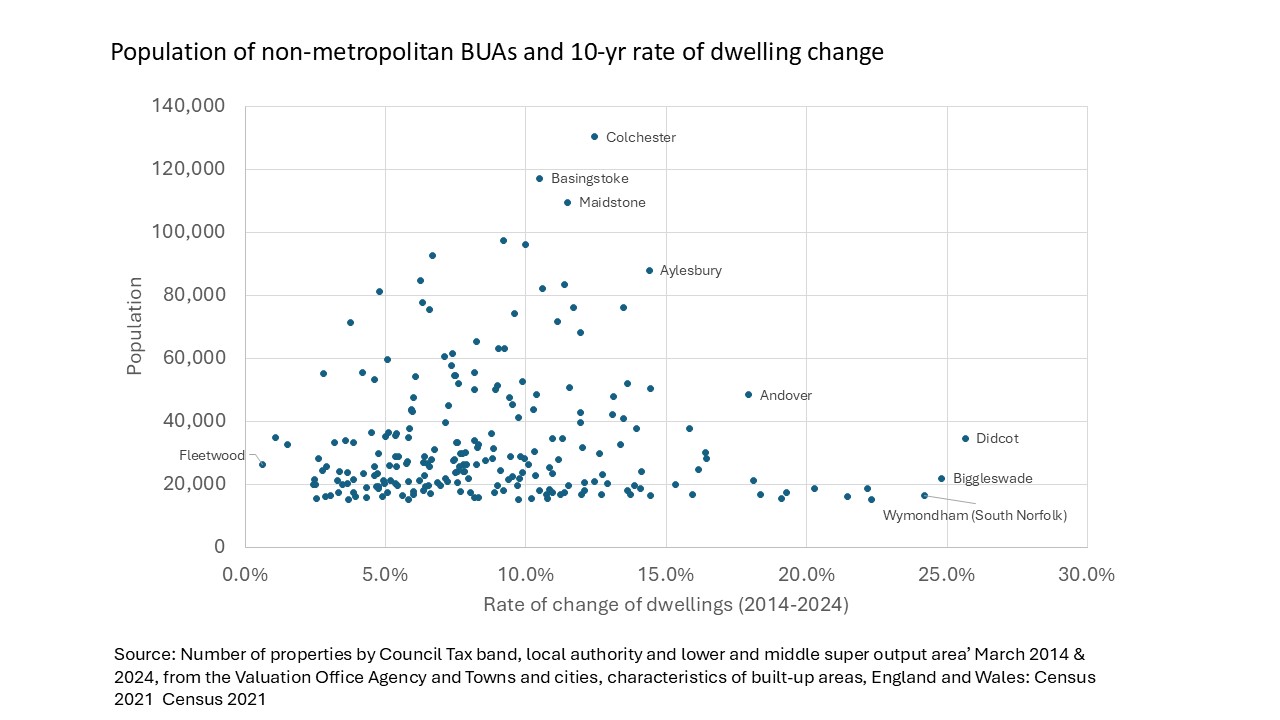

Examining settlement size alongside housing growth shows that larger towns and cities added more homes in absolute numbers, contributing significantly to housing delivery. No correlation was found between the rate of housing delivery relative to size, indicating that housing growth is evenly distributed rather than concentrated in larger and better-served non-metropolitan settlements.

Given the quantum of housing delivered non-metropolitan areas clearly play an important role in national housing delivery, though no clear pattern of growth across settlement size raises questions about infrastructure provision and how spatial planning and market forces guide housing delivery.

Delivery rates of flats and terraces in non-metropolitan settlements are exceeding the national average.

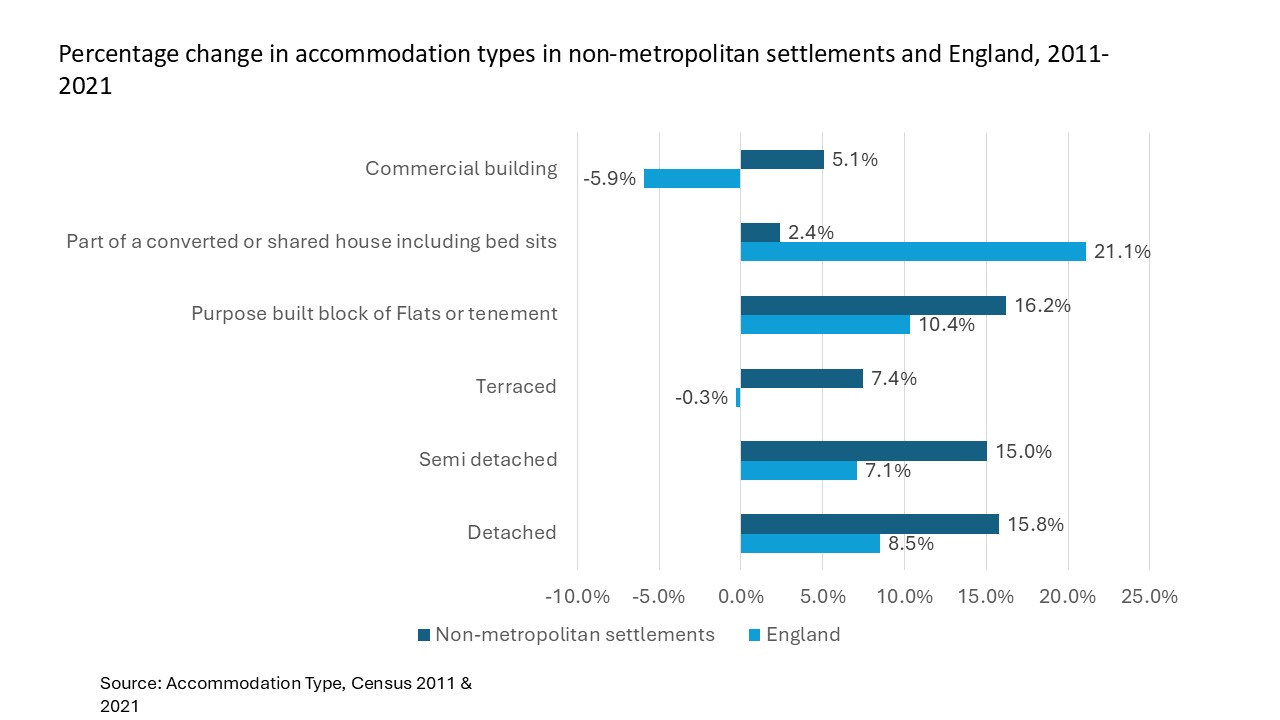

Over the past decade, semi-detached and detached housing has accounted for 70.3 per cent of all new housing in non-metropolitan settlements.

Contrary to common perceptions, higher-density flats are the fastest growing accommodation type in non- metropolitan settlements (16.2 per cent), exceeding the average 10 per cent increase across England.

Additionally, these settlements have seen a notable rise (5.1 per cent) in accommodation within commercial buildings (housing in an office building, hotel or over a shop), contrasting with a national decrease (-5.9 per cent) in this type of housing. This trend likely reflects use of permitted development rights to facilitate sporadic retail-to-residential conversions, alongside more coordinated efforts to repurpose vacant space amid falling office and retail demand.

Non-metropolitan settlements also outperform England in the delivery of new terraced housing (7.4 per cent versus -0.3 per cent), indicating growth in medium-density housing options which runs counter to a decline in this housing typology across the country.

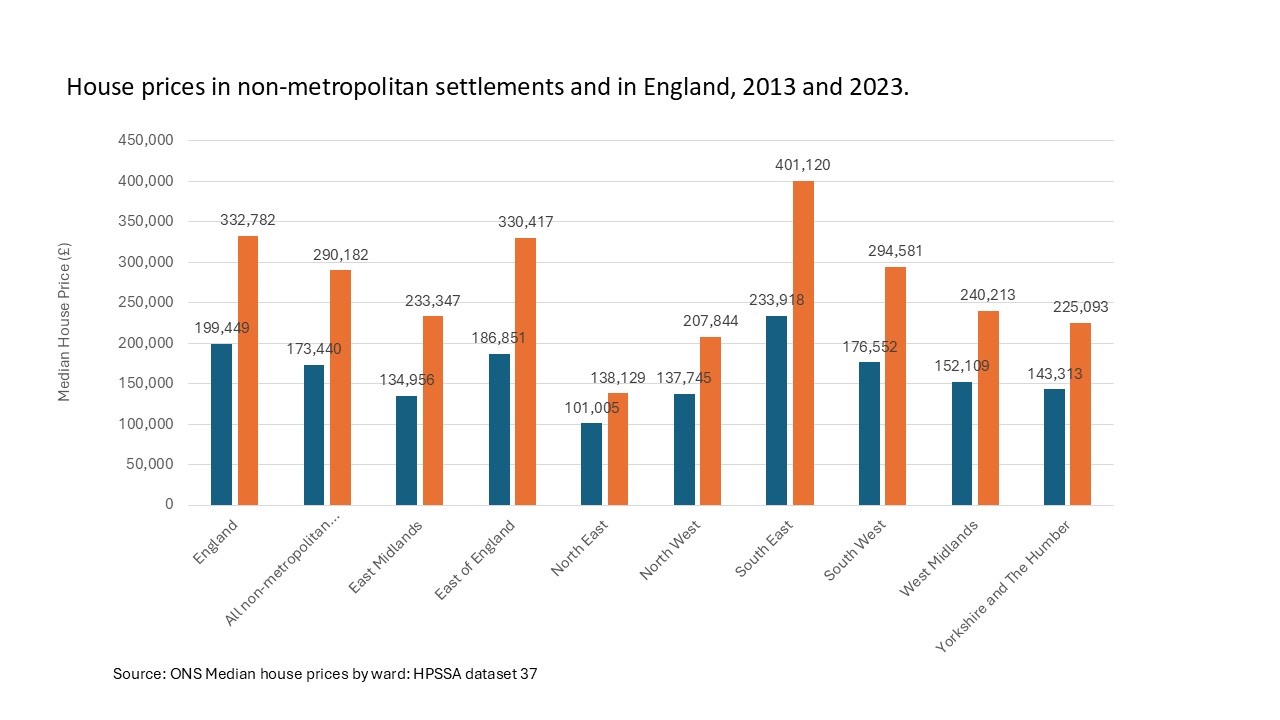

Housing in non-metropolitan settlements is 13 per cent more affordable than the national average.

House prices in non-metropolitan settlements have increased at the same rate as the England average, both experiencing a 67 per cent increase over the decade.

On average, house prices in these areas are 87 per cent of the national median price, with this affordability gap remaining constant since 2013. The East of England, East Midlands, and South East, experienced the strongest median price growth.

Conversely, the West Midlands, Yorkshire, North West, and North East all experienced below-average price growth in non-metropolitan settlements, resulting in their affordability relative to England improving over the decade.

These findings indicate that non-metropolitan areas maintain a consistent affordability advantage, although slower regional growth may reflect broader economic challenges.

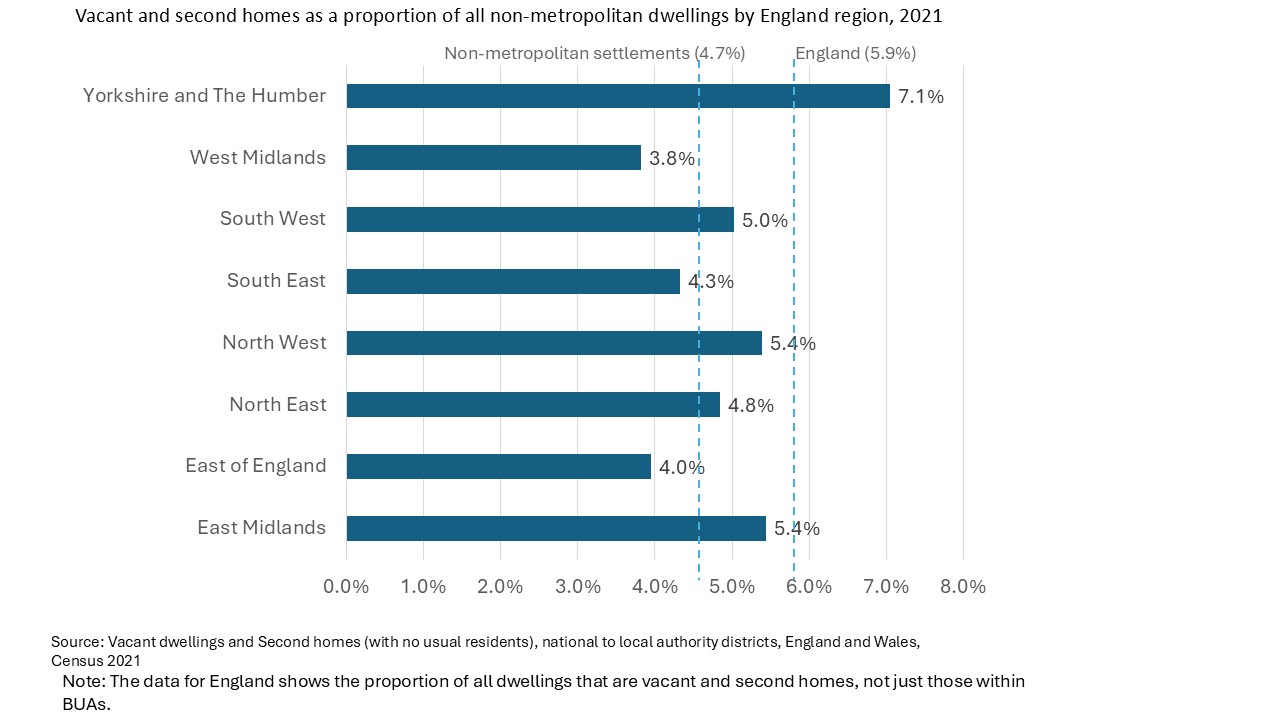

Almost 5 per cent of homes in non-metropolitan settlements are vacant or second homes

There are 170,600 vacant houses and second homes in non-metropolitan settlements in England. These account for 11.3 per cent of the over 1.5m vacant housing and second homes across the whole of England. Across all regions, vacant homes account for a much greater proportion than second homes.

The distribution of vacant and second homes is reflective of non-metropolitan housing distribution and are concentrated in the South East, East of England, and South West.

Vacant and second homes disproportionately affect non-metropolitan settlements in the North of England. Yorkshire and the Humber is most impacted with over 7 per cent of all housing in non-metropolitan settlements being vacant or second homes, an average of almost 1,190 vacant and second homes per non-metropolitan settlement. Yorkshire and the Humber also has a much larger proportion of second homes than other regions.

Vacant housing in and around town centres is a significant issue that impacts on vibrancy and undermines regeneration efforts.

In the graph below, the England average represents the proportion of all housing that is vacant or second homes (including rural areas), not simply those in Built Up Areas, so it is expected that there would be a higher proportion of vacant and second homes. We expect higher levels of vacant and second homes in rural areas, which are included within the England average, but are not included in the averages for non-metropolitan settlements.

Conclusions

Non-metropolitan settlements play a vital role in England’s housing delivery, accounting for one in seven homes. They offer greater housing diversity and choice, with nation-leading rates of flat and townhouse delivery. These areas typically exhibit higher rates of home ownership and maintain more affordable housing compared to the national median. However, regional disparities in growth and affordability, alongside a lack of concentrated development in larger settlements with better services, underscores the need for targeted infrastructure and planning strategies to support continued development outside urban centres.

- Significant housing stock

Non-metropolitan settlements account for one in seven homes in England, housing nearly 7.6 million residents in 3.6 million dwellings. This represents 14.2 per cent of all housing across the country.

- Robust housing growth

Over the past decade, non-metropolitan areas have delivered 315,500 new dwellings, although with significant regional variations in delivery. This growth accounts for 14.5 per cent of England’s total new housing supply.

- Diverse housing options

These settlements have seen delivery rate of flats increasing by 16.2 per cent compared to the national average of 10 per cent, emerging as the fastest-growing non-metropolitan housing type, enhancing housing diversity and choice.

- Affordable living

Housing in non-metropolitan settlements remains 13 per cent more affordable than the national median house price, an advantage that has held steady over the decade despite house prices increasing by 67 per cent nationally over this period. There has been greater housing delivery in areas with lower house prices. This highlights the important role of non-metropolitan areas in providing housing that is affordable.

Case studies

Introduction

Following on from the data analysis, a more extensive research exercise was undertaken to better understand the motivations and mechanisms for delivering housing in England’s town centres.

This section contains nine case studies examining housing delivery in England’s non-metropolitan areas. Selected from the 226 identified non-metropolitan areas, these examples were chosen for the quality, ambition, or originality of their housing plans. The case studies represent a diverse mix of political control, regional locations, and economic conditions, offering a comprehensive snapshot of council-led housing delivery across England.

To better understand the motivations and mechanisms driving housing delivery, interviews were conducted with senior council leaders in regeneration, planning, and housing roles. These interviews provided rich insights into the role of councils in enabling housing supply and revealed distinct approaches, challenges, and successes in different contexts.

Each case study follows a structured format to ensure consistency and comparability. They provide a place profile, an overview of the town including key socio- economic and town centre performance metrics, a planning, policy and governance section, summarising how these have contributed to successful housing delivery. On overview of the council’s approach to housing delivery and detail on key projects is provided, and other town centre regeneration projects are summarised. Lessons on how councils have delivered housing and regeneration projects are identified from each case study.

The case studies set out in this section are all examples of places where the council has enabled housing delivery in their town centres, or has plans to do so in the short-term. The scope of intervention ranges from creating the environment for housing delivery through planning policy through to direct intervention via self-delivery.

However, the case studies vary considerably in terms of the baseline circumstances and built form of the town centres, with a mix of older and newer towns, a mix of struggling and robust retail centres and a spectrum of economic and deprivation profiles across the nine examples.

The interview process also revealed that while all of the councils saw housing delivery as a means of enhancing their town centres on some level, the motivations for introducing housing, the scale of delivery and the scale of Council involvement in realising these visions were often very different.

While the case studies present a range of recent experience, from councils who are directly delivering high-density town centre housing to councils who simply aim to guide small-scale delivery, there are some overarching lessons that can be drawn from this exercise. These are summarised in the conclusion section.

Case study 1: Lancaster, Lancaster City Council

Lancaster’s development reflects a careful balance of heritage preservation with growing housing needs. The council has successfully used policy to ensure the highest possible quality and to manage the quantum and type of housing. Lancaster has fully embraced the opportunities presented by student housing and has sought to futureproof itself against future market changes by ensuring the flexibility of its developments. The council is being proactive in advancing housing proposals as part of a major, mixed-use regeneration scheme – The Canal Quarter - in partnership with the private landowners, where previous private-sector led schemes have fallen through.

Place profile

Lancaster is a cathedral city in the North West of England, with a population of 53,000, making it functionally more like a town. It is part of the group of 13 historic cities in England with rich heritage dating back to its heyday as a Georgian port. Lancaster is distinctive in having a very large student population, with two universities based in the city Lancaster University (based at an out-of-town campus at Bailrigg) and the Bowerham Road campus of the University of Cumbria (on the periphery of the city centre). As of the 2021 Census, 50 per cent of Lancaster Central MSOA were students.

The city has seen a 10 per cent increase in housing stock over the last ten years and had previously exceeded its statutory housing target, although it currently does not have a 5-year housing land supply.

Market context and challenges

Lancaster’s city centre has shown resilience compared to similar areas. Pre-pandemic, commercial rents were rising sharply; however, a combination of affordability and pandemic-enforced closures led to a doubling of vacancy rates in the early 2020s. Whilst vacancy rates are still above Lancaster’s long-term average, rents are beginning to recover and the average letting time is now relatively short at just under 4 months as of 2024. Lancaster has seen business growth in the centre and investments such as the Health Innovation Campus.

Planning, policy and governance

The city’s development is underpinned by the Lancaster District Local Plan, which was adopted in 2020 and is currently under review. The plan identified a ‘broad location for growth’ in Bailrigg, South Lancaster, which included provision for a garden village, but rising construction costs have stalled this project, prompting a review of the Local Plan. There is no dedicated town centre strategy for Lancaster, but there is a detailed Supplementary Planning Document for the Canal Quarter.

Local plan policies prioritise city centre brownfield developments and set requirements for high-quality development, driven by conservation area designations and a comparatively high proportion of listed buildings in the city. The Lancaster City Council Homes Strategy 2020-25 also earmarks the city centre as one of the most appropriate locations for new student housing development.

The council has introduced an Article 4 direction across Lancaster and neighbouring village of Galgate, restricting permitted development rights and preventing the conversion of housing residential units to HMO without having to apply for planning permissions.

Housing delivery

Lancaster faces land constraints to where houses can be developed due to the two areas of National Landscape (formerly Areas of Outstanding Natural Beauty), an area of Green Belt, flood risks, and severance of the city centre from adjoining residential areas caused by the gyratory road network. These factors have driven a town centre and brownfield-first approach, which has been the focus of local plan policies for some time in Lancaster, as well as nearby Morecambe, where land is more readily available in the town centre.

Successful and high-quality private sector-led schemes have revitalised industrial sites along the Lune River. The main criticisms have been that, in some cases, they have failed to deliver sufficient mix of uses. With most city centre brownfield sites having been regenerated, the council has allocated greenfield sites on the edge of the city, such as a ~750 homes being brought forward by Taylor Wimpey in North Lancaster and ~900 homes by Persimmon in East Lancaster.

Student housing

Lancaster has seen a significant uptick in the total amount of purpose-built student accommodation, with the Local Plan supporting student accommodation developments on the campus and within the city centre. Recent student developments have included Caton Court (630 beds), Luneside (431 beds, completed 2020) and the two most-recent City Block developments; a conversion of the listed former Gillows building (96 beds) and a new-build scheme over new commercial units at Marton Street (58 beds), which replaced a former public house.

Future developments approved or under construction include the Primus development (388 units) which will complete in 2025, and purpose-built housing for the University of Cumbria’s campus (214 units).

Within the conservation area, the preference is for the retention of ground floor units for common-residential use, ensuring vibrancy and provision of mixed uses. Architecturally, the student schemes have been of a high design quality, even those outside of the conservation area, such as Caton Court, a high-quality brick and stone development.

Given uncertainties around the quantity of student housing needed and levels of future demand, the council requires developers to evidence that their scheme are capable of reversibility and being converted to other uses.

The council is also seeking to direct students into purpose-built student housing and preserve and free-up residential housing stock in the city centre and nearby residential areas by enforcing an Article 4 Direction. This restricts the conversion of residential units to HMOs without having to apply for planning permission

Canal Quarter

Lancaster City Council are spearheading plans for the residential-led regeneration of the Canal Quarter, which is the city’s last remaining major brownfield site (16 acre). A Masterplan was approved in 2023 and seeks to guide the delivery of housing, additional business space, an enhanced arts and cultural offer and the restoration of some of the heritage assets within the Quarter, including the former Mitchell’s Brewery. Early phases of housing could, subject to planning permission, include an affordable housing development at the Coopers Field/St Leonard’s Gate part of the Quarter, and similar development at the southerly Nelson Street. The Canal Quarter is partly owned by the council, with council-owned car parks included within the boundary, and partly owned by private sector developers. The council is collaborating with the developers to integrate their proposed schemes.

The council has taken a more proactive role in delivering the site following previous private sector schemes that failed to progress over a decade ago. The council has been successful in securing Brownfield Land Release Funding to help unlock the Canal Quarter site. (The Brownfield Land Release Fund (BLRF) is a cross-government initiative between the Department for Levelling Up, Housing and Communities (DLUHC) and One Public Estate (OPE) which is delivered in partnership by the Local Government Association and the Cabinet Office).

Morecambe

In the nearby town of Morecambe, innovative schemes by developer Place First have reconfigured and transformed underused housing into one- and two- bedroom flats across the West End One (107 units) and Bay Mill (42 Built-to-Rent units) schemes, providing housing that is responsive to local market conditions.

The council has in recent years taken ownership of the former Frontierland amusement park after a series of private sector proposals failed to emerge. The council has launched a tender process to invite bids from commercial leisure, hospitality and mixed-use developers to provide a comprehensive leisure and tourism focussed development to complement Eden Project Morecambe which will be built near to the Frontierland site. The Eden Project Morecambe scheme was awarded £50 million through the Levelling Up Fund Round 2, and is currently in the delivery phase, helping to reimagine Morecambe as a seaside resort for the 21st century.

Lessons

Planning, policy and governance

- Ensure high quality development with relevant Local Plan policies and leveraging the heritage context to enable planners to enforce the highest quality.

- Consider the new government housing targets within their local contexts. The new targets are particularly difficult in Lancaster as most city centre brownfield sites have been redeveloped, and targeting out-of-town greenfield sites may not generate desired outcomes (for example, car dependency) without significant public and active transport infrastructure delivery.

Housing delivery

- Council intervention may be needed for schemes where private sector plans have repeatedly failed, to bring together various private sector interests.

- Prioritise a town centre and brownfield land-first approach to housing delivery to regenerate under-utilised sites (including council-owned car park) and strengthen the vibrancy of the city centre.

- Require developments that are flexible that can be adapted to meet fluxes in market, such as student housing schemes that can be converted to standard housing.

- Leverage the opportunities provided by student housing and be intentional about delivery of student housing, controlling the quality and stock. Focus student housing in purpose-built blocks rather than residential houses, through an Article 4 directive preventing housing being turned into HMOs and student housing without planning permission.

Town centre regeneration

- Retain ground floor units in city centre sites for commercial activity, to deliver a mix of uses, while being pragmatic and flexible on the possible types of uses that can be accommodated.

Case study 2: Telford, Telford and Wrekin Council

Telford is currently seeing high density housing delivery in its town centre, as well as the delivery of family housing and some conversion of upper floors of retail units to housing. The council is playing a prominent role in much of this development, with its arms-length housing company Nuplace a significant partner in town centre housing delivery.

Despite proposals for large-scale densification, Telford’s primary town centre does not struggle from a lack of a diverse offer or minimal footfall. The motivation for large-scale town centre redevelopment is instead about assuring the correct types of housing in the correct locations, ensuring a high-quality mixed use offering and de-risking the centre as a future market for Build to Rent (BTR).

Place profile

Telford is a New Town in Shropshire, West Midlands, which was established in the 1960s. The town benefits from its location in close proximity to Birmingham and Wolverhampton by rail and is an employment centre in its own right with a particular focus on manufacturing.

While Telford has heritage assets and older areas nested within its borders, its town centre comprises a 1960s central business district next to Telford Central Station and, as such, does not have sensitive heritage assets which might complicate housing delivery, as seen in many non-metropolitan towns.

Telford has experienced significant growth in its overall housing stock over the past ten years (16.3 per cent) and is one of the few examples of a major non-urban area that regularly meets or exceeds its statutory housing target, with a very high score against the Housing Delivery Test (264 per cent).

Market context and challenges

Telford town centre (defined as the central shopping area next to Telford Central Station) has a low vacancy rate and has been very resilient to footfall variation in recent years, with a 2024 retail vacancy rate of 0.5 per cent - very low by the standards of England’s high streets.

Although occupancy rates in the centre dropped by 1.2 per cent during the pandemic, this equates to a vacancy of just 11,000 sq. ft.- a very small decline compared to other town centre retail areas in England. As of late 2024, occupancy rates have recovered to within 0.2 per cent of pre-pandemic levels. The town centre’s health may partly be due to its diverse uses, with an already-established leisure and retail offering, unlike many older towns. For example, the Southwater development was completed in 2014 and encompasses an ice rink and cinema, as well as retail and commercial space, representing an early example of developing a more “experiential” town centre.

As shown, Telford is seeing most of its housing delivered on suburban sites and via urban extensions. However, there are also a number of town centre developments which have been recently completed or are under construction, with council-led schemes forming an increasingly large component of new delivery. In particular, the council is delivering transit-oriented medium-density development in the town centre in the form of the Station Quarter. Elsewhere, Telford has delivered more typical family housing in sites bordering the town centre, as at Southwater Way, as well as projects to redevelop the upper floors of retail units as housing in centres, such as their 1 Walker Street project in the historic district centre of Wellington.

For a long time, Telford & Wrekin Council struggled with delivering private market rental properties of a high quality. This is partly because Telford isn’t an established market for BTR or other specialised private rental operators (unlike in nearby Birmingham) while having significant demand for private rental properties. Consequently, the council identified a significant shortfall of private rented accommodation of a reliable quality which met high environmental standards or catered to specific groups. In 2015, Nuplace was established by the council as arms-length housing delivery company to plug the gaps in the market.

Planning, policy and governance

Telford & Wrekin Council has been under consistent leadership (Labour) since 2011. The council successfully bid for national levelling up funding, having been allocated £22.3m from the Towns Fund in 2021.

Telford’s Town Investment Plan (TIP) included projects across the town’s local centres, such as urban design improvements to the Place Theatre at Oakengates, the refurbishment of historic buildings in Wellington town centre and the delivery of a new “digital skills hub” at the Station Quarter. Bringing forward new housing was a strong feature of the bid.

Housing delivery

A significant share of market rent homes in the borough have been delivered by the council, with Nuplace the largest private sector landlord in the borough. As of early 2024, Nuplace had a portfolio comprising 485 homes with a further 359 units in delivery. The majority of Nuplace’s developments delivered to date are in suburban or out-of-centre locations. However, the past few years have seen a shift towards delivery in Telford town centre, where Nuplace is the most prominent housing developer.

As a company owned by the public sector, Nuplace has a number of objectives beyond simply delivering high quality new homes. The company also aims to raise the overall standard of private renting across the Borough, generate a long-term income stream for the council (to protect frontline services), regenerate brownfield and stalled sites and stimulate local economic growth through job creation. In addition to generating construction jobs, Nuplace makes extensive use of local supply chains, with most suppliers based within a 30-mile radius of Telford town centre.

Nuplace has a management model similar to that of a commercial housebuilder, with long-term partnership arrangements with private housebuilders (in this case a strategic partnership with as regional volume housebuilder across multiple projects). Likewise, for more conventional plots, Nuplace delivers pre-designed housing products, where capital costs are predictable and bespoke elements are minimised. The delivery structure relies upon a 100 per cent council borrowing structure, with affordable tenures cross-subsidised by private tenures. In terms of leadership structure, the company has sought to keep a small core team with industry skills developed through private sector experience.

Southwater Way

2022 saw the completion of 46 homes on Southwater Way on the edge of the Town Centre. The project was delivered as part of a joint venture between Nuplace and a major regional housebuilder, with grant support from the West Midlands Combined Authority.

50 per cent of the units are 3-4 bed family housing units, with all homes built with in-built roof solar PV panels and EV chargers provided - beyond the environmental requirements for new housing at the time. Southwater Way was delivered via Nuplace’s standard delivery approach, with NuPlace funding the delivery of the scheme which was designed and constructed by the partner company.

Station Quarter

Station Quarter is a mixed-use, housing-led development encompassing more than 700 new homes, a hotel, commercial units and an education and digital skills hub on a site next to Telford Central Station. The first phase of the project started on site in January 2024, which comprises 189 homes, with Nuplace delivering 117 largely 1 and 2 bed units and a housing association delivering the remaining 72 affordable units.

Station Quarter is intended less as a boost to the town centre (which has healthy footfall and low vacancy rates) and more as an early venture into higher-density BTR housing in Telford. Nuplace aims to create a new market for town centre living and in so doing derisks and sets the quality for any future higher-density development on the part of private BTR operators. Similarly, the mixed use and education-focussed nature of the scheme, which will see the relocation of Telford College to the centre from a peripheral location, aims to meet other strategic objectives for the council beyond housing delivery, such as assuring greater graduate retention in the town.

The development was openly tendered on a two-stage process and will be delivered with additional grant funding support via the national government’s Levelling Up Fund and Towns Fund, as well as funding from the Marches LEP.

The prominence and sensitivity of the site has meant that Nuplace has needed to vary its standard approach to housing delivery. For example, a more specialised housing developer has been appointed to lead the apartment block component of the development and another for the family housing element, rather than a single house-building partner across the whole site. Likewise, a Masterplan was delivered for the site with Design Code elements, which is in contrast to Southwater Way and other Nuplace projects, where pre-applications were the primary means of setting the format of development.

The apartment component is being marketed at multiple groups such as young professionals with jobs served by the nearby railway station, as well as older existing residents who are looking to downsize their properties. On-site completion is targeted at Summer 2026.

Lessons

Planning, policy and governance

- Put in place a specific Masterplan to be to enable delivery of higher density housing in the very centre of town.

Housing delivery

- Leverage large-scale town centre development to enable wider regeneration objectives (such as enhancing graduate retention in the town) and to deliver housing types which largely aren’t delivered by private developers.

- Establish an arms-length housing company to deliver market-rate housing in town centres and address a lack of private rented housing.

- The success of the arms-length housing company can be attributed to its purposefully lean development model based around strategic partnerships with housebuilders, with minimised staffing and design costs and a portfolio approach to funding and debt management.

Case study 3: Aldershot, Rushmoor District Council

Aldershot is an example of a town centre where its retail offer could not be relied on alone to ensure its vitality. As part of an integrated and coordinated intervention, Rushmoor Borough Council strategically bought a number of vacant town centre retail properties to develop a larger housing-led mixed-use proposal through a strategic partnership with a private developer.

The council has not only financially invested in one of the key town centre schemes but has also played a proactive role in attracting further private investment and securing critical central government funding to bring forward both council-led and third-party projects.

Place profile

Aldershot is a mid-sized town in the London commuter belt which falls within the Borough of Rushmoor. In terms of its economic and demographic profile, Rushmoor has average deprivation levels but household incomes and house prices which fall above England-wide average values. The council is notable for having significantly exceeded its allocated housing target, as demonstrated by the above Housing Delivery Test metric.

As of 2024, Aldershot has higher than average retail vacancy levels in its town centre and lower than average retail rent values per square metre.

Market context and challenges

A number of major retailers left prominent sites in the town centre during the early 2010s, with the town centre’s retail offer considerably compromised and large parts suffering from high vacancy rates.

Likewise, the town faces significant barriers to private development in that there are low overall returns to property development, given low rents and sales values. At the same time, build costs are high due to the town’s location in the South East of England.

In common with many other non-metropolitan towns, there is enormous demand for private rented accommodation on the part of key workers and other groups. However, there were few opportunities for established PRS developers to enter the market, with a limited supply of large or easily consolidated sites and the lack of an established market for private rented accommodation in the town centre.

While the town faced significant decline of its established retail offer, there were opportunities for repurposing the town centre. The University for the Creative Arts Farnham (UCA Farnham) was identified as having the potential to help reinvigorate the town centre through a greater student and creative presence. Likewise, while not an established commuter destination, Aldershot has a relatively good rail connection to employment centres in London, while having the benefit of lower house and rental prices than other rival markets in the South East of England.

Planning, policy and governance

In 2016 the Aldershot Town Centre Prospectus was developed and adopted as a Supplementary Planning Document, but purposefully written for a less technical audience. This was developed at an early stage of the council’s plans for town centre regeneration and was intended to sell the potential of a repositioned and reimagined town centre. The document was developed in close collaboration with the local community and stakeholders, with the Prospectus an outcome of significant private and public sector engagement. The document set out the council’s objectives including to cultivate town centre living, enhance the cultural offer and to diversify the centre through both renewed retail and other non-retail uses.

In 2019, the council adopted the Rushmoor Local Plan formalising key development opportunities in the Prospectus document as site allocations in Union Street East (Union Yard) and The Galleries.

Establishing a robust planning position helped to unlock government funding for the Union Yard scheme in the form of £5M from the Housing Infrastructure Fund, alongside £1.2M from the Enterprise M3 Local Economic Partnership. The Galleries scheme was also supported by £3.4m from the Housing Infrastructure Fund to help with site remediation and infrastructure delivery to unlock the site.

Housing delivery

A joint venture between the council and Hill Investment Partnership (jointly, the Rushmoor Development Partnership) was formed in 2018, with the Partnership initially looking at four key sites across the borough, including two major town centre sites in Aldershot and Farnborough with the opportunity to unlock in excess of 1,000 new homes.

While the Partnership structure is one of shared risk and reward, different arrangements have been in place for different developments, with the council leading the delivery and taking the financial risk of the Union Yard project. The Galleries project sits outside of the Partnership and is led primarily by the private landowner, Shaviram Group.

Union Yard

Union Yard is a council-led regeneration project nearing completion on the site of multiple former retail units between Union Street and High Street in the heart of town centre. The scheme includes 128 student units, 18 affordable homes aimed at those aged 55 and over, and 82 market-rent apartments, offering a unique mix of housing options that will introduce a diverse range of residents to the town centre. The Rushmoor Development Partnership secured the planning consent but, in this instance, the council has taken forward the scheme as landowner with Hill appointed as contractor for the build.

The development incorporates commercial space suitable for the town’s needs, including makers spaces for small or independent businesses alongside ground-floor retail units engaging onto a newly designed public square and established retail frontages on Union Street. The maker spaces are provided in the form of container units, which provide a smaller, temporary and more affordable space for local creatives to sell their products, with larger retail units available nearby in the event of wanting to scale-up.

The mid-rise character of the development has taken into account the surrounding historic context through a carefully considered design and use of materials.

The Galleries

The Galleries is a separate privately-led development located nearby, which aims to deliver 596 apartments on the former site of a shopping mall. Spread across several buildings and rising up to 12 storeys, the project is currently in the early phases of development with demolition and site clearance well progressed following planning approval in 2022.

The Galleries development aims to function harmoniously with Union Yard, with the scheme offering a fundamentally different format of retail offer, focused more on flagship tenants, compared to Union Yard’s independent retail focus.

Rushmoor Borough Council owns the freehold of part of the site and it is being brought forward by the Shaviram Group. The council will release the site to Shaviram at the point of delivery of a new 250-space public car park on a separate plot to serve the town, which will be transferred into council ownership upon its completion.

Wider town centre regeneration

In addition to addressing the oversupply of retail at the Galleries, the council has sought to concentrate retail in the heart of the centre and away from the periphery of the town through a relaxing of retail frontage designations in the Local Plan, resulting in a much smaller share of the town being designated for retail uses.

The council is also embarking on large scale regeneration in other Borough-wide town centre sites. Farnborough Civic Quarter, a 960 unit mixed-use development has secured outline consent, with other uses such as a hotel, leisure and non-residential floorspace also planned for the site. Further development of the site may be conditional on national government funding and this is actively being explored.

Lessons

Housing delivery

- Reboot the town centre offer by balancing a bold and ambitious strategy and carefully considered long-term partnerships with the private sector.

- Constant adaptation of developments to market circumstances, with a pragmatic mindset on the part of the council. Adapting of delivery arrangements needed to factor for the changing investment landscape.

- Negotiation of build costs at a fixed price prior, insulating the development from build cost inflation.

Planning, policy and governance

- Planning frameworks play a crucial role in assuring buy-in and achieving consensus. An integrated Prospectus functioned as both a statutory planning document and a public-facing document to promote the council’s town centre vision.

- Strong and new council leadership provided a bold vision and the political support to see its long-term plans come to fruition.

Town centre regeneration

- Maximise the potential of town centre investment by integrating multiple policy goals, such as delivering student and private market housing and temporary retail, enabling local makers to sell their products in a low-cost space.

Case study 4: Hereford, Herefordshire Council

Hereford has seen recent town centre residential development in the form of in-fill residential development and student housing in its historic core. It has ambitious plans going forward with proposals for key worker and specialised housing on other town centre sites, with the council playing a significant role in delivery.

The recent set of proposals for town centre residential development are a response to longer-term housing targets, the need for new and specialised forms of housing and to achieve longer-term diversification of uses in the centre. While the decline of retail in the centre is a factor and is being addressed by wider place-making strategies, town centre regeneration is not primarily being pursued for this reason. Given the heritage restrictions of the centre, new town centre development has had to be pursued sensitively and collaboratively through a Masterplan-led planning strategy.

Place profile

Hereford is an historic cathedral city and the county town for Herefordshire Council. The town is not demographically similar to other traditional English county towns, in that it has a relatively high working age population and has house prices and incomes below the England average.

It has seen above average overall increase in housing stock in the ten years to 2024, and has notably seen a significant share of its housing delivery in the town centre (as well as on the outskirts), which is not typical of many rural English towns.

Market context and challenges

Hereford has relatively low retail vacancy rates, at around 4 per cent of total retail space in 2024. However, the town has suffered greater from the cost-of-living crises and lack of consumer spending than other areas, with vacancy rates doubling in the last two years. This is more concentrated in certain parts of the centre, with the Maylords Shopping Centre seeing the loss of two anchor tenants, with the centre eventually bought

for further redevelopment by the council. In line with this trend, over the same period the average cost of town centre rents has fallen by 25 per cent, with the average unit taking almost nine months to let. There are more positive signs on the horizon with lettings activity starting to rise again and average town centre rental costs starting to recover to their pre-pandemic levels.

Herefordshire Council has a high overall housing target which is set to rise with the reorganisation of housing targets under the new national government (with the target likely shifting from 16,000 to 27,000 units).

Hereford is necessarily the focal point for new housing development given its location as the largest town in a very rural constituency and a major employment hub.

At the same time, Hereford town centre is not an established location for purpose-built apartments, with the area an untested market compared to larger nearby cities, with most new housing delivered as suburban family homes on the periphery.

Hereford also suffers from significant development constraints, with a small historic centre which experiences significant transport issues due to the flow of commercial traffic through the town centre (rather than via a ring road). As such, parking is a sensitive issue for new development. The council has sought to expand its centre through targeted redevelopment of the former Cattle Market as a new edge-of-centre retail destination in 2014. This in turn has enabled neighbouring vacant sites to become viable as sites for denser town centre housing (as per Merton Meadows, as set out below).

Planning, policy and governance

Hereford is led by Herefordshire Council- a unitary authority.

A draft Hereford City Masterplan was produced in Spring 2023, which set out core growth objectives for the city and centre, including enabling a “a vibrant historic core”, with plans for delivering housing as part of the Owen Street Quarter. The Masterplan is intended to guide the form, tenure and mix of uses on sensitive town centre sites, so as to ensure greater local buy-in. The council is in the process of updating this plan to reflect the new NPPF guidance and mandatory Housing targets.

To unlock aspects of their long-term strategy for the town centre, Herefordshire Council applied successfully for £20 million in funding to deliver its Hereford City Transport Package project as part of the Levelling Up Fund Round 2. This included schemes such as public realm, pedestrian and cycling infrastructure improvements and a new transport hub at Hereford Railway Station. The town received a further £22.4m in funding to deliver its Town Deal via the Towns Fund Programme, with projects including a new Digital Culture Hub and Skills Centre, a new public library, a refurbished Hereford Museum, an electric buses project and provisions to enhance the biodiversity and green credentials of the centre.

To unlock aspects of their long-term strategy for the town centre, Herefordshire Council applied successfully for £20 million in funding to deliver its Hereford City Transport Package project as part of the Levelling Up Fund Round 2. This included schemes such as public realm, pedestrian and cycling infrastructure improvements and a new transport hub at Hereford Railway Station. The town received a further £22.4m in funding to deliver its Town Deal via the Towns Fund Programme, with projects including a new Digital Culture Hub and Skills Centre, a new public library, a refurbished Hereford Museum, an electric buses project and provisions to enhance the biodiversity and green credentials of the centre.

Housing delivery

Herefordshire largely relies on the private sector to deliver much of its housing, but is looking to take a greater lead working directly and with Partners to enable more specialised forms of housing in the centre to meet unmet demand, such as purpose-built homes for the over-55s and key worker housing. Herefordshire also has a very large housing waiting list (around 2500 on the list in 2024), with significant affordable housing delivery considered the most economical long-term solution to this. As a means of achieving these goals and enabling future development, Herefordshire Council has been proactive in unlocking major town centre brownfield sites. At Merton Meadows, the council will employ national government funding to address long-term flooding problems, which will make the site a more attractive and viable proposition for new housing.

However, Hereford town centre doesn’t have a large resident population, and the council has not been able to rely on the private sector alone to deliver all of the types of housing needed, such as high-quality key worker and retirement homes. Therefore, Hereford is currently in the process of establishing some form of public housing delivery body (whether a joint venture or a standalone council-led ALMO). The company will aim to set the standard for new types of housing in terms of quality, aesthetics and tenure mix, to enable high quality private development to eventually deliver housing of a similar calibre.

Merton Meadows

A council-owned city centre gateway site. As of 2024, the site is prioritised for up to 400 dwellings, with a focus on delivering intergenerational housing for retirees, as well as key worker housing, based around a highly landscaped setting. The council-owned site is currently going through masterplanning and will likely be delivered with a commercial partner or through a new arms-length housing delivery vehicle. The site has received more than £2m in funding from the national government’s Brownfield Land Release Fund to remediate flooding issues, which is crucial for the activation of the site.

Wider town centre regeneration

Herefordshire Council’s town centre vision sees greater housing delivery as just one of multiple holistic measures to enhance the centre. As part of a longer-term strategy to diversify the uses of the centre,

Hereford successfully attracted the New Model Institute for Technology and Engineering (NMITE) to permanently locate to the town in 2021, bringing activity and realising the town’s longer-term ambitions as a centre for higher education. In order to facilitate this move, Herefordshire Council released some of its publicly owned land near the railway station to be delivered as student housing by a private developer. 178 units were delivered at Station Hill in 2021.

Similarly, Hereford sought to expand its city centre and retool its retail offering through the development of the old Cattle Market as an edge-of-centre retail destination in 2014.

Lessons

Town centre regeneration

- Delivery of high-quality retail, employment, education, health, leisure and amenity offers alongside new residential developments has been needed to encourage people to live in the centre.

Housing delivery

- However, ensuring the delivery of the right type of town centre housing is often a necessary prerequisite for a major rethinking of town centre uses. In the case of Hereford, delivering student housing was vital for attracting a higher education provider to the town.

- Consider the most appropriate housing types for town centre locations. Accessible town centre sites in Hereford considered most appropriate for key worker and certain types of retirement housing.

Planning, policy and governance

- Use public assets such as railway station and gateway sites pragmatically to unlock delivery of town centre housing.

- Use SPDs to set the tone and ensure design quality of new buildings in town centre developments. This is especially the case for historic towns with development restrictions and where town centre housing is a largely new phenomenon.

Case study 5: Folkestone, Folkestone and Hythe District Council

Folkestone exemplifies how cultural initiatives and clear vision through a place plan can revitalise a town centre. Folkestone and Hythe District Council have been proactive in incentivising, delivering and coordinating a spectrum of regeneration interventions, and establishing a platform for investment.

It has taken an active role in addressing issues of development viability by remediating challenging sites and partnering with developers to reduce risk. The council also leverages its wholly owned housing company, Oportunitas, to provide new housing to meet growing demand for private rented housing.

Place profile

Folkestone, a town on the Kent coast, has experienced a remarkable transformation after a prolonged period of decline common to many coastal areas. This revival has been driven by ambitious development plans and substantial investments, spearheaded by local philanthropist Sir Roger De Haan. Cultural and art-led regeneration initiatives by Creative Folkestone have changed the town’s image and appeal, making it increasingly popular among young renters. London commuters have been relocating to Folkestone in large numbers due to the direct, high-speed train link.

Market context and challenges

A growing population has increased the demand for housing, leading to a surge in rent prices. The prevalence of Airbnbs and second homes exacerbates the shortage of housing and affordability issues, and contributes to a transient population, with some properties occupied only on weekends.

Folkestone faces stark socio-economic disparities and deprivation that persists in certain areas of the town. These inequalities are heightened by the town’s changing demographic. Tied to this are the growing issues of a lack of affordable housing and high waiting lists for council homes.

However, the delivery of additional housing is constrained by challenging brownfield sites requiring significant remediation and the antiquated road network. This puts pressure on the viability of sites, which is being further impacted by rising interest rates and building costs.

While the Old High Street is performing well due to interventions from Creative Folkestone, there are high vacancy rates at the top of the high street in the direction of the station and in the main retail core, where flagship retailer Debenhams closed in 2020.

Planning, policy and governance

Folkestone’s development is guided by a comprehensive Place Plan, which laid the foundation for a successful Levelling Up Fund bid. This bid addresses a number of public realm and connectivity challenges, especially around the station area leading through to the town centre. Folkestone also recently underwent a rebranding campaign to raise awareness of its transformation, particularly aimed at London audiences.

The council has implemented measures to streamline the housing approvals process, specifically for Housing Revenue Account (HRA). By producing an HRA pipeline report approved at the cabinet level, the council can deliver housing schemes within the set parameters of the business plan without needing cabinet approval for each project. This approach has enhanced responsiveness to market needs and developer interest.

The council engages regularly with key stakeholders leading the development of Folkestone, notably organisations backed by Sir Roger De Haan. Through its planning functions, the council seeks to facilitate and enable investments.

Housing delivery

Housing stock has increased by 7 per cent in the last 10 years. Most new housing has been delivered in the town centre and on the western edge of the town. The delivery of housing is motivated by a need to provide suitable housing for a growing population, increase the provision of affordable housing, particularly as house prices are rapidly rising, and future-proof the town centre.

Folkestone’s housing delivery features several key projects:

- Shoreline Crescent: Up to 1,000 new luxury flats on the seafront, including the recently completed first phase comprising of 84 flats. The Folkestone Harbour & Seafront Development Company (FHSDC), led by Sir Roger de Haan, oversees this £1 billion initiative to regenerate the harbour area.

- Ship Street (Old Gas Works): A challenging site between the station and the seafront that has been unused since the 1960s. The council’s ambitions plans for regeneration include 134 units and enhanced public realm.

- Live-Work Units: Units on the old High Street have been converted to creative Live-Work units. These have had significant positive local impact on vibrancy.

- Vacant Floors above shops in the High Street. A local developer has taken over a stalled project to deliver in excess of 30 units in the town centre.

- Royal Victoria Hospital Conversion: The old hospital building was converted to 18 high quality flats together with a brand new block of 19 flats, overlooking Radnor Park, just minutes from the station. All 37 units were acquired by the council’s housing and regeneration company – Oportunitas.

- Biggins Wood Brickworks Site: This site, vacant since the 1970s, has been remediated by the council to create a development platform. The council is in the process of disposing of the site which has planning permission for 77 houses and 5,600sqm of commercial and office space.

- Highview Site: The council purchased an old school which has since been demolished and is being prepared for sale, having received planning permission for 30 homes.

Several models are being pursued by the council for the delivery of housing and regeneration projects.

The council is actively delivering new homes through Oportunitas – a company wholly owned by Folkestone and Hythe District Council – that was set up to deliver more homes for the private rented market. As of late 2024, Oportunitas owns 75 properties, including one commercial unit. It aims to offer affordable rents in the future as it transitions into profitability.

The council is proactive in incentivising developer interest by de-risking projects, particularly on more challenging sites. One way the council is doing this by remediating brownfield sites using funding from government like brownfield land release funds, and in some cases, acquiring planning permission, before disposing of the site to a developer or partnering with a developer to bring forward much needed homes.

A second way that the council is de-risking challenging projects is by taking on the delivery of part of a scheme. The council is considering how to enable the regeneration of the Old Gas Works site on Ship Street site, which faces issues of viability due to the need

for remediation, challenging gradient of the land, high retaining walls and surrounding property values, as it is in a more deprived part of the town. The council is planning on retaining the affordable homes for the HRA and exploring the potential of whether a proportion of units could be taken on by Oportunitas – the council’s housing company for private rent. This will further de-risk the site for incoming developers as they won’t need to find a provider for the affordable homes, and will pay tranche payments, reducing the amount of capital borrowing by the developer.

Effective partnership working and an active approach to stakeholder engagement has been a key strength of Folkestone’s housing delivery. The Old Gas works site was activated as part of the Triennial in partnership Creative Folkestone and the council have used innovative approaches to stakeholder engagement including the use of VR headsets to reach a wider audience.

Wider town centre regeneration

A comprehensive approach to regeneration links multiple projects across the town:

- The council has acquired the former Debenhams building which has been rebranded as ‘Folca’ to prevent landbanking of this key site and plans to repurpose it for mixed-uses, including a GP surgery and leisure facilities, subject to business case viability. However, rising costs, rising interest rates on loans, and requirements for building energy efficiency standards pose a number of challenges.

- The Old High Street revitalisation: Led by Creative Folkestone, which acquired many properties and rents them at reduced rates for creative uses, including Live/Work creative spaces.

- Levelling Up Fund – ‘Folkestone a Brighter Future’. A £20M investment targeting public realm improvements, improvements to the main gateways to the town centre and high-street and connectivity enhancements.

- Old Harbour Regeneration: The Harbour Arm has been transformed by the Folkestone Harbour & Seafront Development Co. into a vibrant area with F&B and leisure uses.

Lessons

Planning, policy and governance

- A clear plan and vision, such as Folkestone’s Place Plan, provides strategic direction for the town’s development and helps to unlock funding from central government.

- Branding initiatives can help to change the perceptions of a place, raise awareness, encourage new residents and drive tourism. Folkestone’s recent branding campaign has contributed to its changing image, promoted the investments into the town, and attracted new residents from London.

Housing delivery

- Local councils can take an active role in de-risking development projects, making them more attractive to investors. Councils can do this by leveraging external funding, remediating sites or taking on a part of the development, reducing the capital investment for developers.

- A pipeline of HRA projects approved at the Cabinet level can speed up delivery of housing and make a council more responsive to market demand, enabling a council to deliver projects within set parameters, rather than requiring approval on a project-by-project basis.

Town centre regeneration

- Council acquisition of key town centre sites – such as the former Debenhams building – can prevent landbanking of the site by developers and deliver much needed facilities to the town centre.

- Mixed use redevelopment of vacant retail assets incorporating modern medical and leisure facilities can be used to encourage footfall to the town centre.

- Reduced fixed rates from government on loans for regeneration and housing projects, particularly HRA housing, would give local authorities the tools to undertake regeneration projects in the context of rising interest rates and challenging viability.

Case study 6: Bognor Regis, Arun District Council

Bognor faces two significant challenges: the restoration of its heritage assets, and the ongoing challenge of attracting footfall to the town centre, having previously been a popular seaside holiday destination. To help address these issues, privately rented housing is being incorporated in plans to restore a key heritage and retail asset in the centre – The Arcade -, as a means to aid project financial viability and create an ongoing investment asset. The council-led project has allowed for a longer-term view on its social and economic benefits. Nonetheless, housing alone is not seen as a "silver bullet". The council is prioritising complimentary culture, tourism, and leisure-driven regeneration through its wider assets to enliven the town centre.

Place profile

Bognor Regis, situated on the South Coast within Sussex's Arun District Council, is a medium-sized town with a unique character and heritage assets. Unlike Brighton, Hastings, or Folkestone, Bognor Regis has not seen significant growth in population or housing over the past decade, with housing stock having increased by only 5 per cent.

Market context and challenges

The town centre of Bognor Regis has faced significant challenges in recent years. The effects of the pandemic on the retail sector were notable and more recently, the cost-of-living crisis has had a profound impact, with constrained householder spending contributing to commercial vacancy rates skyrocketing sixfold in the past two years. Over 11,000 sq ft of lettings have been lost. Despite these challenges, rents in the town centre have remained high, suggesting a potential for rebalancing affordability to restore vibrancy. The town’s identity as a tourism and leisure destination has waned, with insufficient hotel and leisure facilities for short stays having contributed to the decline in visitor numbers. Albeit this has been partially addressed with the recent sale of brownfield sea front land by the council to Whitbread who are currently constructing a new Premier Inn on the site. The council are also evaluating two other potential hotel sites which they may bring forward for development if viable.

One of the principal shopping centres in Bognor Regis is the Arcade, holding a collection of 21 units occupied by predominantly independent retailers and Food & Beverage outlets. The upper floors were previously office chambers but are currently unoccupied and in an extremely poor state of repair. The council acquired the centre in 2017 but its heritage status (locally listed) and the future costs of repairs and maintenance represent an additional challenge in maintaining this asset as purely commercial/retail/office (for which there is little demand).