Executive summary

High streets have evolved over centuries as civic and commercial centres for their communities, playing a central role, figuratively and literally, in the economic and social life of towns and cities.

Town centres have faced challenges as demands have changed and options opened up. Vacancies in many high streets have grown in the face of economic headwinds as local consumers have less to spend and an increasing preference for online retail and retail parks where larger, newer stores are easily accessible by car. High streets and shopping centres have struggled to recover from the impact of COVID.

Central government has made a number of changes councils are managing.

- Commercial use classes. There have been a number of changes in use classes in recent years. The largest of which was the creation of use class E in August 2020, a new ‘commercial, business and service’ use class incorporating the previous class A uses. For many units this removes the need for planning permission for previous changes of use These changes are broadly welcomed by the private sector who value the flexibility, but the public sector are less positive, concerned by the loss of power to control the types of uses.

- Permitted development rights. Since 2013, the Government has gradually expanded the remit of permitted development rights, as a way of speeding up the planning system. In August 2021, permitted development rights were expanded to reflect the introduction of the new use classes order and to encourage residential development. This means that buildings falling within use class E (commercial, business and service) have the right to change to residential use (use class MA). These changes have also been broadly welcomed by the private sector while the public sector has been opposed, seeing residential conversion as potentially undermining existing high street recovery plans and providing poor quality housing with no S106 contribution.

- Article 4 directions. These are legal tools that local councils can use to restrict permitted development rights, such as converting commercial properties (class E) into residential (class MA). This requires full planning permission, allowing councils to consider wider planning issues including to protect town centres from the negative impacts of excessive residential conversions, such as loss of shops and businesses, which can undermine their vitality.

The Levelling Up and Regeneration Act (LURA) 2023 includes provisions that councillors will be able to consider in strategies to improve their high streets and town centres. These include:

- Local rent auctions. LURA 2023 empowers local authorities to hold rental auctions for vacant properties in designated high streets and town centres. This aims to address landlord inaction and bring vacant units back into use. There are concerns about the practicality and resource demands of local rent auctions.

- Mayoral development corporations. These entities, led by combined authority elected mayors, have increased powers to regenerate areas, including compulsory land purchase and development control.

A number of announced and potential future initiatives from the central government will impact local high streets and town centres and their improvement strategies.

- Continued support for a plan-led approach: Both the current and previous governments emphasise a plan-led approach to development, with the updated NPPF strengthened to this effect. There were no changes in NPPF guidance for high streets.

- Support for high streets in the Budget: The 2024 budget allocated £1 billion to revitalise high streets and confirmed funding for Levelling Up Fund projects. It also introduced permanent changes to business rates to benefit smaller retail, hospitality, and leisure businesses.

- Focus on local growth plans: The government aims to encourage the development of local growth plans, integrating spatial, transport, energy, and skills planning to drive local growth.

- Brownfield planning passports: A proposed initiative aims to streamline development on brownfield sites through ‘brownfield passports’ and the wider use of local development orders. This approach could have a significant impact in town centres.

The changes that being introduced generally reduce the controls councils have at their disposal to stop things happening. However, best practice has shown that the key to a successful high street strategy is positive engagement, encouraging all those with a stake in a centre to work towards a common vision. The key to successful town centres, and dealing with these changes, is therefore the development of clear local policies and strategies that can attract in investment and the desired uses.

Best practice has shown that these strategies need to be well articulated and supported locally, but it is also essential that they reflect the economic and social realities they operate in. They also need to be flexible to adapt to the unforeseen changes that will inevitably arise during any plan period.

Introduction

This independent report has been commissioned by the Local Government Association (LGA) to look at how recent and impending planning policy changes at central government level affect local high street strategies. It has been prepared by Lambert Smith Hampton.

The report aims to improve understanding of the importance of our high streets and town centres and how local government can support them, in the face of significant changes in society and our economy.

Challenges for our high streets are not new – the LGA published a report over a decade ago entitled ‘Alternative high street - rethinking the town centre challenge’ which notes in its introduction:

For better or for worse, our town centres are changing; responding to powerful socio-economic trends driving shifts in retail behaviour. Locally, there is consensus among town centre partners that new approaches are needed to ensure high streets adapt successfully

The report goes on to note:

But it is crucial that we begin to think more positively about the challenge facing our town centres. Retail is not the future, and town centres are adapting. We have to go back to the start, moving beyond retail, and refocusing places as centres of social, community and cultural economies. This is our vision for the alternative high street…. Retail is still important, but as part of a wider community offer.

The intervening decade has seen considerable research on the causes of the structural changes in our high streets and the effectiveness of both local and national initiatives to help high streets and town centres adapt to the scale and speed of change being experienced. However, throughout that time there has been a consistent message from central government through the NPPF, that the planning system should be genuinely plan-led. This requires local authorities to prepare up-to-date development plans for their area, with a specific requirement to support the role of town centres through appropriate planning policies.

In addition to local plans, some local authorities have developed more detailed strategies and planning policy frameworks for their town centres including action area plans, masterplans and other forms of supplementary planning documents. Town centre strategies and plans have also been developed to support applications for funding from central government, who have introduced a number of funding programmes to support town centre proposals.

However, at the same time, central government has also made changes to national planning policies and procedures which have the potential to affect the way local planning policies apply in practice, or make them obsolete. The specific emphasis of this report is to identify the key changes that have been made in recent years and consider how they may affect the strategies and policies being prepared and applied at a local level.

The report also seeks to consider the extent to which the new government may continue with or change the policies and approaches of the previous government, based on its manifesto, the October 2024 Budget and other announcements made to date (November 2024).

The report therefore seeks to:

- Explain the context for central and local government policy interventions in terms of the role of town centres (Section 2) and recent market and economic trends (Section 3);

- Summarise recent changes in planning policy by central government aimed at supporting high streets and consider their effect (Section 4). This section also considers the extent to which changes in approach can be expected as a result of the change in government; and

- Identify key learnings (Section 5).

Original research and case studies are provided throughout the report.

The role of high streets and town centres

Our network of high streets and town centres has developed over many centuries as the focus for commercial and business activities. Each high street has its own unique history and offer but all have the common factor that their mix of uses has developed to meet the needs of the communities they serve.

During most of this time centres have developed and adjusted to the changing needs of the businesses and communities who use them, incrementally. Their original location has also influenced subsequent development and easy access to centres has been reinforced over time as new development has occurred along the main approach routes. The result is that today high streets and town centres are the focus of our transport systems, making them the most accessible locations for most communities. In turn this attracts both footfall and a wide range of business interests, continuing their important role economic and social roles.

The introduction of a land use planning system in the mid-twentieth century recognised the importance of town centres in our society and planning policies have given specific consideration to town centres from the outset, whether considering land use, transport and accessibility, heritage or any other aspect of the planning system.

From the 1970s onwards, technological advances and social changes saw a significant rise in the demand for new commercial floorspace and an increase in the size of unit required. In retail this reflected the growth in the weekly bulk food shopping trip, whilst new technology was requiring larger footprints for office accommodation.

In some cases this led to major redevelopment proposals coming forward in town centres, resulting in larger scale development often in a single ownership. Retail and, to a lesser extent office development dominated and led to the position where town centre and high streets became synonymous with shopping.

However, the scale of retail expansion was greater than could be accommodated in central locations and the development of out of centre retail, leisure and business parks became common. Whilst market sectors were generally growing, concerns started being raised about the impact of out of centre retail development and policy support for town centres at a national level was first introduced in 1996. This introduced a ‘town centre first’ approach to development and required compliance with the sequential test for retail, leisure and office development. This means locating retail and other main town centre uses in town centres, then in edge of centre locations and, only if suitable sites are not available within a reasonable time period, should the development of out of centre sites be considered.

However, the last decade has seen major changes in society and customer behaviour, with some of these trends and effects compounded by the Covid-19 pandemic. This has included (but is not limited to) growing online sales, increased living costs and falling disposable income, higher business costs and increased working from home.

Town centres are also seeing the longer term effects of improved personal mobility which has increased accessibility to a greater range of centres. Residents in one area are no longer restricted to centres they can walk to or get public transport to and the result is that high streets and town centres are in competition with each other, both for customers and new businesses looking to locate in an area. As a result, the pressures and challenges facing our high streets and town centres are not coming solely from out of centre competition but also from each other, and it has to be recognised that any uplift in trade in one location is likely to result in a decline elsewhere.

For some time it has been apparent that relying on retail uses for a successful and vibrant town centre is rarely sufficient and both national and local planning policies have increasingly supported a mix of uses in town centres. In many locations some changes have happened organically, with leisure uses such as restaurant and cafe operators occupying space vacated by retailers. However, it is the speed of the changes that has caused many of the recent problems, with the result that many town centres have not been able to adjust quickly enough.

This has led to greater interventions by local and central government in the form of planning policies, town centre strategies and government funding for high street and town centre initiatives. The purpose of this report is to look specifically at how recent national changes to planning policy may affect the high street strategies being developed at local level.

Challenges facing Britain’s high streets

The last 5 -10 years have been a very difficult period for the retail industry. Changing economic, consumer and property market trends have led to structural changes in the retail and leisure sectors and will continue to shape change in the future.

The UK economy

The UK economy in terms of gross domestic product (GDP) has seen relatively limited growth during the last 20 years, with GDP per head hit by the 2008 recession and more recently by the Covid-19 pandemic. The post pandemic recovery saw GDP per head peak in Q1 2022 at a level similar to that seen in Q3 2019, but it has been in decline since.

The period since the pandemic has also seen the end of very low interest rates and rising inflation, with the latter peaking in October 2022 at over 11 per cent.

The result is that UK households are currently experiencing the biggest fall in real disposable income and living standards in decades. This has had a direct impact on household spending on retail goods and leisure services, and on the sales performance of retailers and leisure operators.

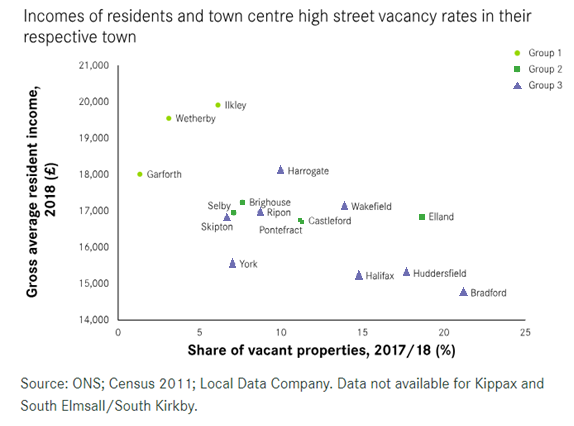

However, economic performance across the country is not uniform and the strength of the local economy will be one of the major determinants of the local high street performance. As a result the areas with the highest vacancies are often located within areas of lower economic performance and incomes. Centre for Cities analysis showed that within West Yorkshire, high streets in areas with the highest average resident incomes of around £19,000 per year had the lowest vacancy rates at around 5 per cent. High streets in areas with average resident incomes of around £17,000 had vacancy rates around 10 per cent, and where incomes were around £15,000 high street vacancy rates reached 20 per cent.

Figure 1: Vacancy and Income Levels – West Yorkshire Case Study

Source: Centre for Cities- What determines the performance of a high street

Business Costs

The pandemic also impacted on the sales and viability of a wide range of retail, catering and leisure formats. Many businesses are still carrying debt and higher interest rates have increased the cost of loans. They have also faced rising operational costs and labour shortages precipitated by the economic downturn since 2022. This has resulted in numerous high profile retail business failures both pre and post pandemic.

Non-store (internet) sales

The growth in non-store retail sales, and principally internet shopping, has had a significant sustained impact on consumer spend and behaviour over the last decade, with direct consequences for the performance of our “bricks-and-mortar” stores. The pandemic accelerated online usage and although online shopping rates have declined slightly since then, the amount of online spend remains significantly higher than at the beginning of the century

The market share of non-store retail sales, as a percentage of total sales, increased from under 5 per cent in 2007 to 30 per cent in 2020 and is forecast to increase to 31.6 per cent by 2030. Online sales for non-food goods is higher than for food.

The internet is also impacting on how and where people choose to spend their leisure time. Not only are consumers increasingly turning to digital platforms for entertainment, including video games and streaming services, social media platforms like Facebook, Instagram, and TikTok with features like shoppable posts and in-app checkout, streamline the purchasing process and make it more convenient for customers, particularly younger generations, to make a purchase.

The use of delivery services for food and drink is also on the rise.

Changing work patterns

Consumer and work behaviour also changed significantly during the pandemic, with more people choosing to work from home and visit local shops and services. In general terms this shift in consumer demand has benefited smaller centres and local neighbourhood locations with strong residential (“walk-in”) catchment populations.

Effect on town centres and high streets

The result of these economic challenges and changing customer behaviour has been a decrease in the number of retailers operating from high street locations, with a number of high profile retailers that were struggling pre-pandemic due to falling sales, increasing costs/debt and poor management going out of business completely or reducing their store portfolio.

Some of the space vacated has been taken up by expanding leisure uses such as food & beverage operators and also a growth in retail services, but vacancy levels have also risen.

Retailers normally associated with out of centre developments are also facing challenges and the closure/rationalisation of their operations has created additional vacant space, providing those few businesses wanting space with greater choice and making it more difficult to let the usually older and more expensive high street properties.

The result is that whilst vacancy rates went up for all locations immediately after the pandemic peaking in mid 2021 rates have fallen fastest in retail parks now at just below their pre pandemic levels at 8 per cent according to the Local Data Companyv. Meanwhile rates in high streets remain close to the pandemic peak vacancy rate at 14 per cent, above the pre-pandemic rate of around 13 per cent.

The strong performance of retail parks reflects the fact that they remain relatively desirable destinations for shoppers and operators due to their convenience, ease of access, free and extensive parking, larger format stores, and their competitive rental values. They are therefore an attractive proposition for those retailers seeking space in the current market, where the need to keep costs down is a major consideration.

The result is that many centres and shopping locations across the UK simply have too much retail floorspace stock, and/or they have the “wrong type” of retail floorspace that does not meet the needs of modern national retailers for larger format shop units.

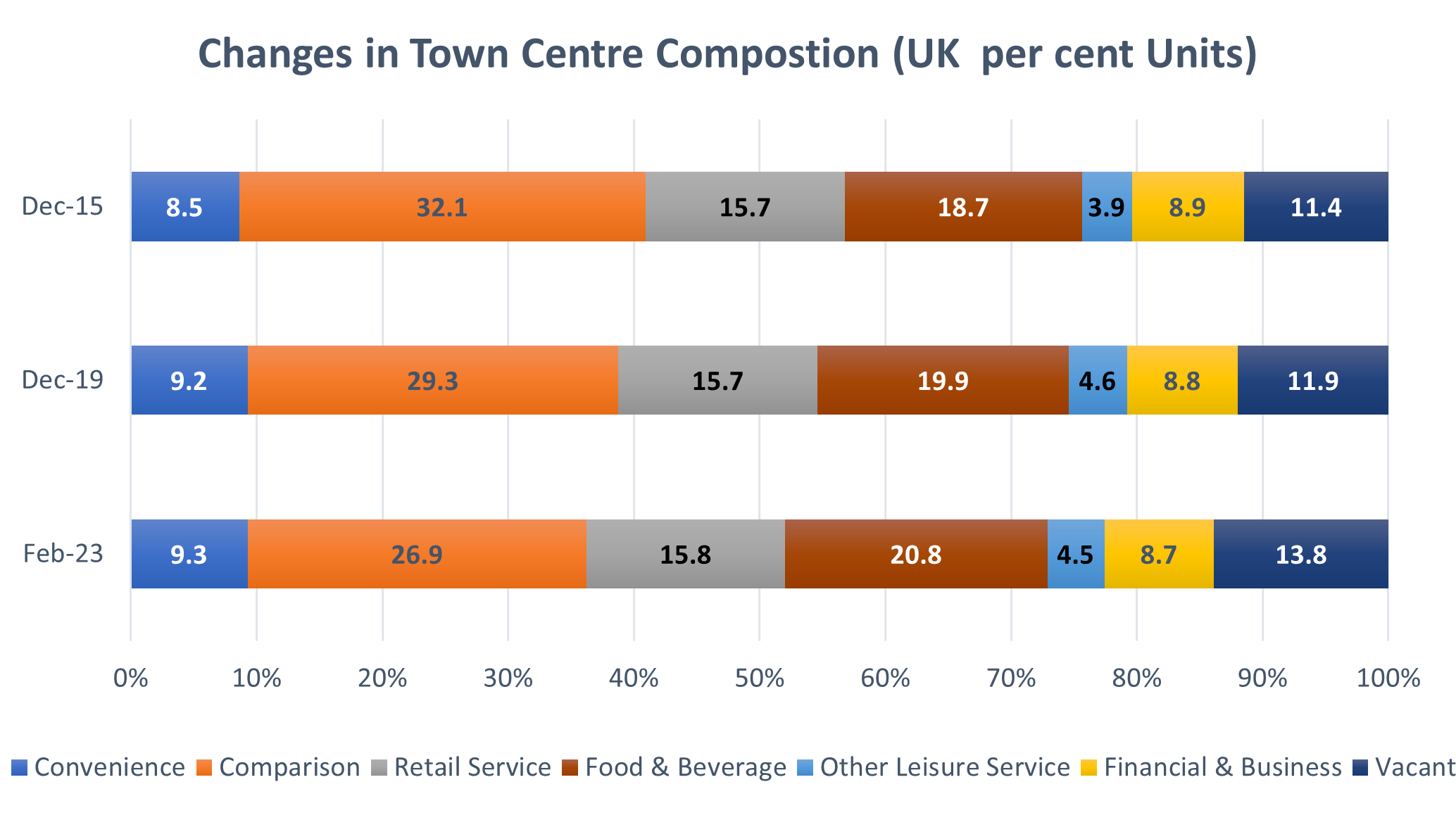

The overall effect of these changes is that the mix of uses in town centres has changed significantly over the last decade, with comparison (non-food) retail provision seeing a decline, whilst convenience retail has increased slightly. Retail services, food and beverage uses and other leisure services have also increased whilst financial and business uses have declined.

Figure 2: Town centre composition (2015, 2019 and 2023)

There will always be a degree of variation between centres, reflecting their history, their role and function and surrounding network of competing centres, but it remains the case that overall the UK’s towns and cities have more retail space than they need. Innovative ideas to rethink, reinvent and repurpose the UK`s towns and shopping centres are needed so that they are fit for purpose in the post-pandemic world.

Central government responses and effects

As the challenges facing our town centres from economic and social changes have increased over time, so has the need to co-ordinate investment and development proposals.

The planning system and the adoption of a plan-led approach to development as required in the NPPF is a very important element of this, and councils have been encouraged to develop positive strategies for their centres (NPPF, paragraph 90).

However, the scale of recent challenges and the speed of change seen has exacerbated the problems being experienced in our centres. Central government has therefore sought to introduce measures to assist, by providing additional funding streams and introducing changes to planning policy at a national level.

The changes to policy and the effect this has or is expected to have for local high street strategies is considered below.

Use classes and permitted development rights

One of the most talked about interventions from central government in recent years has been the changes to the use classes order introduced in August 2020.

The current regulations relating to use classes date from 1987 and have been amended a number of times since. The order groups different uses of buildings and land into use classes and a change of use within a class is not considered as development. It therefore does not require planning permission.

The 2020 changes were introduced to reflect the diversity of uses found on high streets and in town centres and were intended to provide flexibility for businesses to adapt and diversify to meet changing demands, particularly in the immediate aftermath of the Covid-19 pandemic. It was recognised that town centres now seek to provide a wider range of facilities and services and therefore a new use class (class E) was introduced incorporating the previous class A uses.

The single ‘commercial, business and service’ class (class E) therefore incorporates:

- retail shops (previously class A1)

- financial and professional services (previously class A2)

- restaurants and cafes (previously class A3)

- offices (previously class B1)

- medical or health services, principally to visiting members of the public, except the use of premises attached to the residence of the consultant or practitioner (previously class D1)

- creche, day nursery or day centre (previously class D1)

- gymnasium or areas for indoor sport, recreation or fitness, not involving motor vehicles or firearms, principally to visiting members of the public (previously class D2).

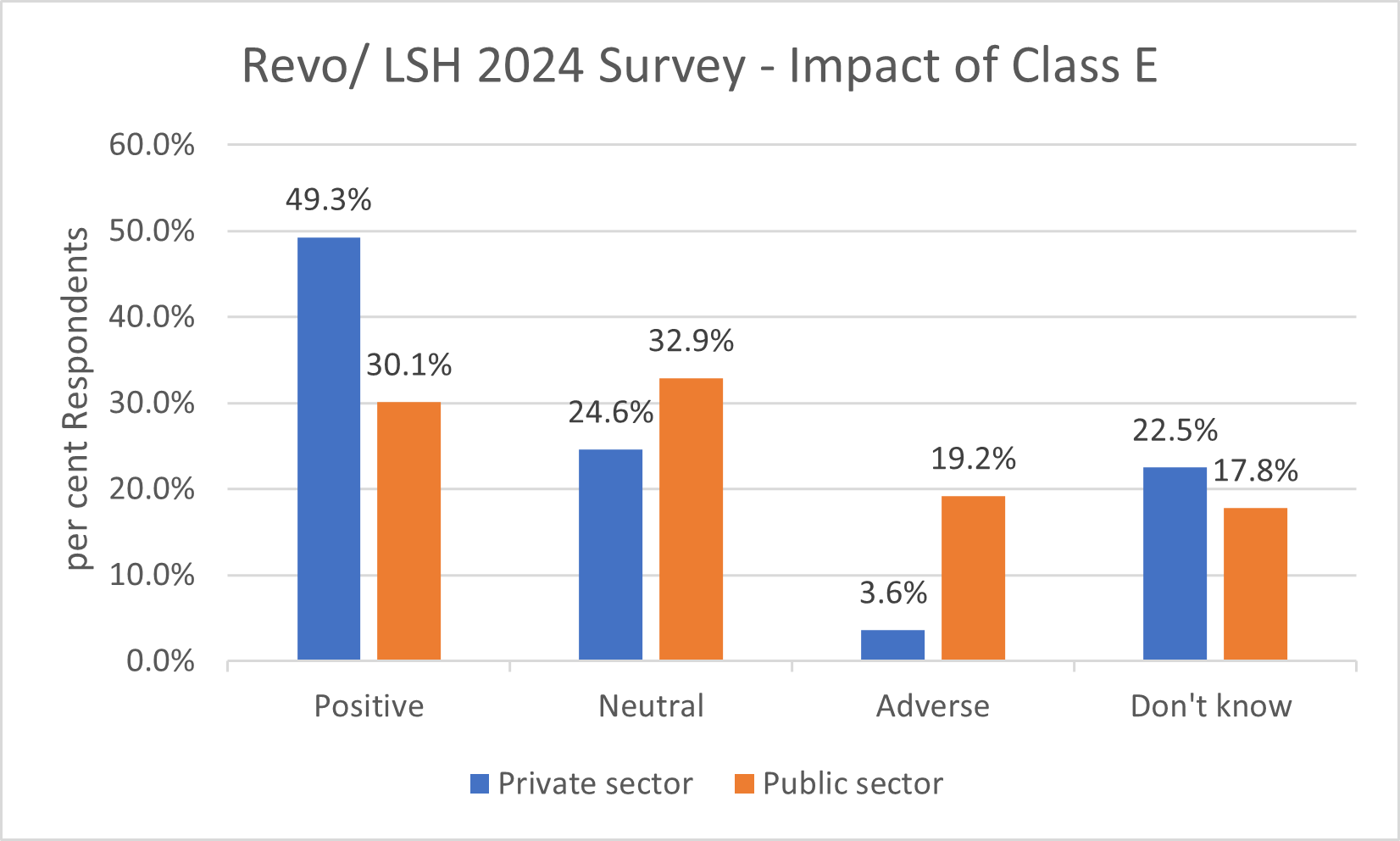

Recent research by LSH and Revo included a survey of key stakeholders and decision makers from across the public and private sectors with a vested interest and investment in the future planning, management and regeneration of the UK’s town centres, high streets and shopping centres. It asked a series of questions regarding the actual and perceived impacts of recent high-profile planning reforms and the Levelling Up and Regeneration Act (LURA) on the vitality and viability of centres and received 211 responses.

A specific question about the impact of the introduction of Class E received a positive response from individuals working in the private sector with 49.3 per cent believing it has had or will have a positive impact. Those working in the public sector were less positive as to its effect with only 30.1 per cent considering it had or would have a positive impact. The proportion believing the impacts have been or will be ‘adverse’ or ‘significantly adverse’ was also higher for the public sector at 19.2 per cent of respondents, compared with just 3.6 per cent of those in the private sector.

Figure 3: Revo / LSH 2024 Survey – Impact of Class E

The main positive benefit of the change is that a wider range of occupiers can now be considered for existing retail units without the owner/occupier needing to obtain planning permission first. This can prove helpful in reducing the length of time units are vacant and has started to attract new uses into centres, such as those relating to health services.

However, from a local policy perspective the introduction of class E has meant that policies which sought to retain minimum proportions of retail uses within parts of town centres have become unimplementable, as planning permission is no longer required to change from a retail use to a café, restaurant use etc.

Where such policies were linked to the need to demonstrate a lack of market demand for the retail use before a change of use would be considered, the change has removed the unintended consequence that restrictions in town centres encouraged some non-retail occupiers, such as restaurant operators, to look at out of town sites. This was because in such locations the change of use application could be submitted at any time, rather than being delayed whilst marketing of the vacant unit was undertaken – when it was often already known that the prospects of finding another retail operator were extremely low.

However, the removal of the need to apply for a change of use has had unintended consequences in some areas, explaining the lower level of support for the introduction of class E in the public sector. This includes:

- loss of retail and active frontage

- impact on residential amenity (e.g. disturbance issues from new restaurants/cafés)

- loss of light industrial

Overall, we conclude that in most cases the new uses permitted in town centres and high streets under class E are not ones that a local planning authority would normally have been likely to resist, as they assist in diversifying the offer and reducing the likelihood of vacant units remaining empty. However, in some cases this change to the use classes could have a detrimental effect on strategies to retain active frontage and in areas of mixed use.

Importantly though, local planning authorities continue to be able to control the main food & beverage uses likely to raise amenity concerns, as both A4 pubs and A5 hot food takeaways became sui generis uses under the 2020 changes. As such planning permission continues to be required for the change to these use from retail or other class E uses.

Other changes to the Use Classes Order 2020

Other changes in the use classes which have received less attention but which also have important implications for our town centres are as follows:

- introduction of a new class F1 (learning and non-residential institutions), which includes some of the former uses under class D1 (non-residential institutions), including museums, public libraries, art galleries, schools, and places of worship

- introduction of a new class F2 (local community uses) includes former class D2 uses (assembly and leisure), such as meeting places/halls, indoor/outdoor swimming baths, skating rinks, and outdoor sport and recreation. A new category of community shop has also been introduced, although this is unlikely to be relevant in high street locations

- an extension to the sui generis uses (which fall outside the specified use classes) to include uses previously classified under D2 (assembly and leisure), including cinemas, concert halls, live music venues, bingo and dance halls. This is in addition to the addition of the former use classes A4 (pubs and drinking establishments) and A5 (hot food takeaways) uses mentioned above.

The changes are summarised in table 1.

Table 1: Use Classes Order – changes in August 2020

| Previous Use Class (up to 31 August 2020) | Use Class (from 1 September 2020) | Description | ||

|---|---|---|---|---|

| A1 | Shops | F2 | Local community uses | Shops not more than 280 sqm mostly selling essential goods, including food and at least 1km from another similar shop. |

| E | Commercial, business and service uses | All other shops. | ||

| A2 | Financial & Professional Services | E | Commercial, business and service uses | Financial Services, Professional Services, Estate Agents, Employment Agencies. |

| A3 | Restaurants & Cafés | E | Commercial, business and service uses | Restaurants and Cafes (excluding Internet Cafes). |

| A4 | Drinking Establishments | Sui Generis | Public House, Wine Bar or other Drinking Establishments. | |

| A5 | Hot Food & Take-away | Sui Generis | Takeaways. | |

| B1 | Business | E | Commercial, business and service uses |

i. Offices, other than a use within Class A2 (Financial Services) ii. Research and development of products or processes iii. Light industry |

| B2 | General Industrial | Unchanged | Use for the carrying out of an industrial process other than one falling in class B1. | |

| B8 | Storage & Distribution | Unchanged | Storage or distribution centre. | |

| D1 | Non-Residential Institution | E | Commercial, business and service uses | Medical or health services, principally to visiting members of the public, except the use of premises attached to the residence of the consultant or practitioner. Creche, day nursery or day centre. |

| F1 | Learning & Non-residential institutions | Museums, Public Libraries, Art Galleries & Exhibition Halls, Law Court, Schools, Non-Residential Education & Training Centres. Places of Worship, Religious Instruction & Church Halls | ||

| D2 | Assembly & Leisure | Sui Generis | Venue for live music performance, a cinema, a concert hall, a bingo hall, or a dance hall. | |

| E | Commercial, business and service uses | Gymnasium or area for indoor sport, recreation or fitness, not involving motor vehicles or firearms, principally to visiting members of the public. | ||

| F2 | Local community uses | Hall or meeting place for the principal use of the local community. Indoor or outdoor swimming baths, skating rinks, and outdoor sports or recreations not involving motorised vehicles or firearms. | ||

| Sui Generis | Other | Sui Generis | Other |

Now includes: Public houses, wine bars or drinking establishments (formerly Class A4) Drinking establishments with expanded food provision (formerly Class A4 or A5) Hot food takeaways (formerly Class A5) Live music venue (formerly Class D2) Cinemas (formerly Class D2(a)) Concert hall (formerly Class D2(b)) Bingo halls (formerly Class D2(c)) Dance Halls (formerly Class D2(d)) Betting offices/shops, pay day loans |

At the time the changes were made, the Government indicated that the introduction of the new use classes order would benefit local planning authorities by reducing the number of planning applications for changes of use they would receive. This would save time and resources and is consistent with other measures introduced to streamline the planning process.

Government statistics for 2023 suggest that the total number of planning applications submitted in England was down around 12 per cent on 2022, which in turn was 14 per cent down on 2021. However numbers submitted in 2021 were 15 per cent up on 2020.

There could be many reasons for this recent decline, but further research would be needed to determine the contribution made by the changes to the use classes order.

Case studies

The benefits of the introduction of class E in diversifying our high streets and town centres can be seen in a number of locations where use class E has allowed flexibility and access to primary retail units for certain occupiers, previously outside of the former ‘A’ use classes, (such as, for example, former class D1 and D2 uses, including the commercial health, beauty and wellbeing sub sectors). This has helped to alleviate vacancy rates in some centres.

The NHS is increasingly taking redundant retail space in shopping centres and high streets locations.

The Mall, Wood Green

In 2022 a new community diagnostic centre (CDC) opened in The Mall shopping centre in Wood Green, London. The centre is run by Whittington Health NHS Trust and offers x-ray, ultrasound, ophthalmology and phlebotomy (blood tests) services to local residents.

The CDC initially occupied two ground floor units which had been amalgamated into a single facility. This has since been extended into a linked lower ground floor unit and MRI and CT scanners have been introduced.

Lister Gate, Nottingham

In April 2024 Nottingham City Council approved plans to redevelop three former retail units at the partly demolished Broadmarsh Centre into a £25m community diagnostic centre for the Nottingham University Hospital NHS Trust.

The facility will provide a "one-stop shop", providing direct access to diagnostics services such as MRI, CT, x-ray, ultrasound, echocardiography, ECG, and lung function testing and is intended to both improve the timescales for seeing patients and help revive the shopping centre.

In this case planning permission was required as the project required the partial demolition of the existing building and the creation of new facades but did not relate to the principle of the use.

Swan Centre, Eastleigh

In 2021 a NHS health hub was opened in a former restaurant unit within the Swan Centre in Eastleigh by the Solent NHS Trust.

The vacant unit was originally identified as suitable by the trust based on its accessible location to the local community and a planning application was submitted in 2019. At that time, prior to the change to the use classes, the proposed use was not considered a main town centre use, but it was recognised that as a complementary use it could support the vitality of the town centre. It was concluded that the health centre would act as a pull for residents to come into the town centre and so provide footfall for the surrounding leisure uses.

Under the 2020 Use Classes Order, planning permission would no longer be required.

Former Marks & Spencer store, Broadmead, Bristol

The inclusion of additional uses within the same class as retail, has also benefitted some proposals for the conversion of larger redundant retail units, such as those vacated by the likes of Debenhams and House of Fraser, as it provides additional flexibility both to attract a range of occupiers and uses and then allow them to adapt to changing demand.

It can also allow ‘meanwhile’ uses to occupy vacant space as has recently happened in Bristol following the closure of the main Marks & Spencer store in the city centre after 70 years of trading.

The vacant unit has been transformed into a temporary art and sustainability centre with a range of shops, installations and events space on the ground floor and a hub for local artists, offering affordable studios, rehearsal and performance space on the first floor.

It provides an active use in a prominent city centre location until the landlord confirms the long term plans for the unit and has been implemented without the need for planning permission.

Permitted development rights

Permitted development rights (PDR) are a national grant of planning permission which allows certain building works and changes of use to be carried out without having to make a planning application. Permitted development rights are subject to conditions and limitations to control impacts and to protect local amenity and are set out in the Town and Country Planning (General Permitted Development) (England) Order 2015, as amended.

Permitted development rights therefore by-pass the local planning authority’s policies contained in its development plan, with the grant of permission only subject to the conditions and limitations set out in legislation.

Class MA (class E to residential)

Since 2013, central government has gradually expanded the remit of permitted development rights, as a way of speeding up the planning system. In August 2021, permitted development rights were expanded to reflect the introduction of the new use classes order and to encourage residential development. This means that buildings falling within use class E (commercial, business and service) have the right to change to residential use (use class MA).

Planning permission is not required for this change of use, but before beginning development under class MA, the developer must apply to the local planning authority for a determination as to whether the prior approval of the authority will be required, due to:

- the transport impacts of the development, particularly to ensure safe site access

- contamination risks in relation to the building

- flooding risks in relation to the building

- impacts of noise from commercial premises on the intended occupiers of the development

- the building being located in a conservation area, and the development involving a change of use of the whole or part of the ground floor. The impact on the character or sustainability of the conservation area is then a consideration

- the provision of adequate natural light in all habitable rooms of the dwelling houses

- the impact on intended occupiers of the development of the introduction of residential use in an area the authority considers to be important for general or heavy industry, waste management, storage and distribution, or a mix of such uses

- the impact on local provision where the development involves the loss of a registered nursery, or health centre

The original 2021 changes to PDR rights also required properties for conversion to satisfy a number of key requirements, including having been vacant for a period of at least 3 months and having a floorspace of less than 1,500 sqm. However, these restrictions were removed in March 2024.

This means that a council’s ability to control the conversion of class E properties to residential use is limited and significantly the impact on the vitality and viability of the retail core or shopping area is not a consideration.

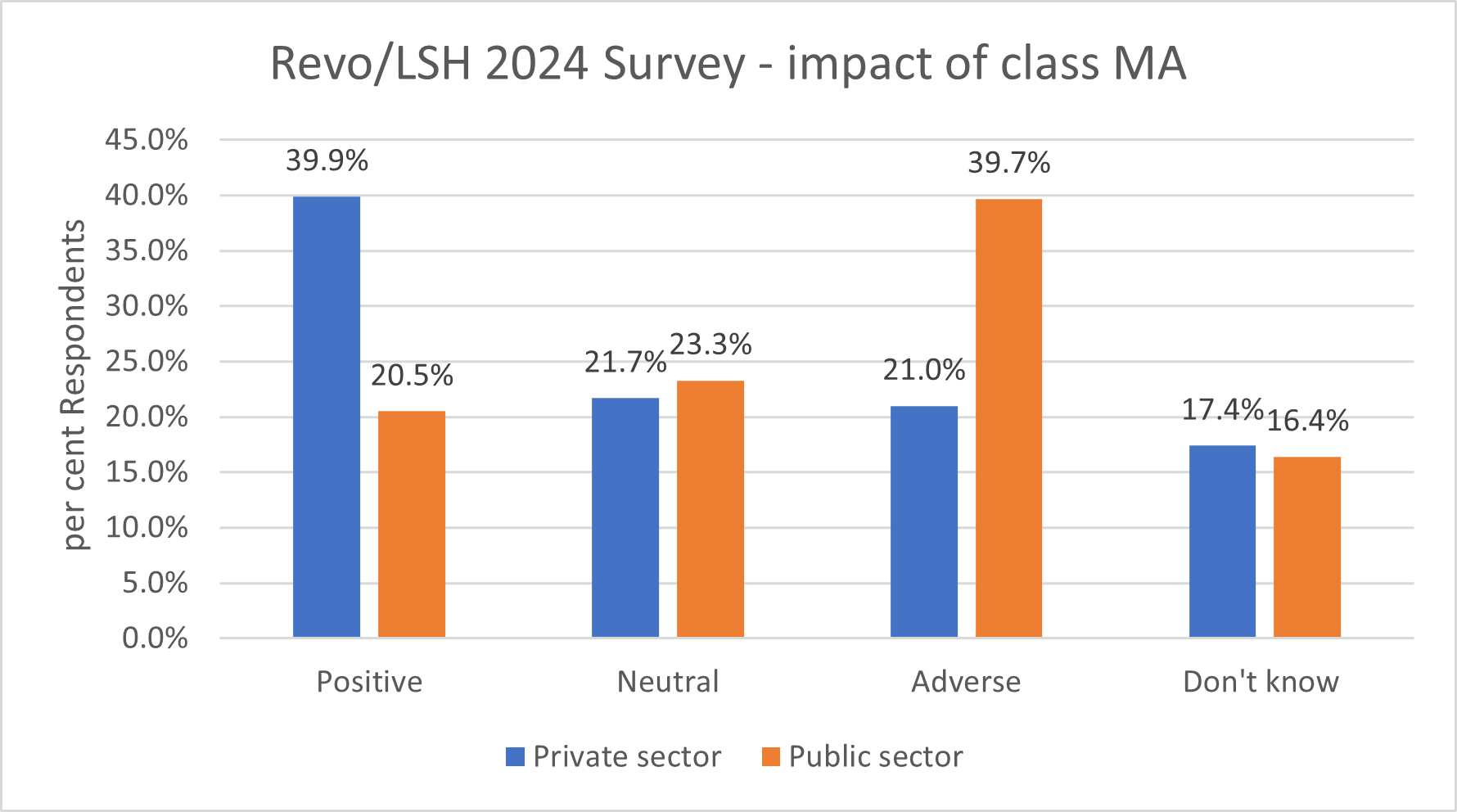

As a result, the response to the question ‘what impact do you think the introduction of class MA to the General Permitted Developments Order (GPDO) in 2021 has had, or will have in the future on the vitality and viability of high streets and shop frontages?’ in the recent LSH / Revo survey received a less positive response than the question relating to the introduction of class E.

Only 20.5 per cent of public sector respondents believed the impacts are or will be positive, while 39.7 per cent consider they are either ‘adverse’ or ‘significantly adverse’. The equivalent responses for private sector respondents saw 39.9 per cent indication they through the change was positive and 21.0 per cent considering it adverse.

Figure 4: Revo / LSH 2024 survey – impact of class MA

The LGA has previously made representations to government consultations explaining why the extension of PDR introducing Class MA were not appropriate, including:

- potential to undermine councils’ existing high street recovery plans, including those benefitting from central government funding initiatives

- loss of active street frontages

- loss of revenue from business rates

- the loss of Section 106 contributions for affordable housing at a time when they are most needed

- increase in poor quality housing

Other permitted development rights changes

The August 2021 changes to the General Permitted Development Order 2015 (GPDO) also introduced a number of other measures that allow specific forms of development to be undertaken under PDR:

- extensions of existing buildings by increasing their height by one to two storey

- the demolition of unused or derelict office/industrial buildings with redevelopment for residential use (class ZA)

Demolition of vacant commercial buildings

The 2021 changes now provide permitted development rights to allow the demolition of some commercial buildings and construction of residential in their place, subject to prior approval. This is currently limited to:

- certain previous uses (office, R&D or light industrial)

- buildings built before 1990

- units that have been vacant for at least 6 months

- buildings with a footprint of under 1,000 sqm, with the rebuild restricted to the same footprint

Possibly as a result of these restrictions, the use of these development rights has been very limited, with government statistics on planning applications indicating just 102 applications in England since April 2021. Of these 79 prior approval applications were allowed and 23 were refused.

The previous government had consulted on a possible extension to these PDRs by removing some or all of the above limitations and the consultation period ended on 9 April 2024. However, there is no indication that the new government are intending to make any immediate changes to PDRs.

Article 4 directions

There is little a council can do to prevent a change from a class E use to class MA, or redevelopment under class ZA once a proposal has come forward, but a local planning authority can restrict permitted development rights in an area under an article 4 direction, named after article 4 of the GPDO.

An article 4 direction removes permitted development rights over a specifically defined area and requires full planning permission to be obtained. This gives the local planning authority scope to consider other planning matters that are within policies in its development plan, rather than only those issues specified by legislation.

A local planning authority can issue an article 4 direction at any time, although these cannot apply retrospectively. There are two types of article 4 direction:

- an immediate direction which removes permitted development rights from the day it is issued, and it can then be confirmed or withdrawn following a consultation

- a non-immediate direction which only comes into effect following a 12-month grace period. This is to ensure the council is not subject to potential compensation claims

The use of article 4 directions is supported by central government subject to it being limited to situations where it is necessary to avoid wholly unacceptable adverse impacts, it being based on robust evidence and applying to the smallest possible geographic area (NPPF, paragraph 53).

The NPPF acknowledges that a wholly unacceptable impact could include the loss of the essential core of a primary shopping area which would seriously undermine its vitality and viability; but notes that it would be very unlikely to extend to the whole of a town centre.

The procedures involved in introducing an article 4 direction include publicising the direction locally and informing the secretary of state by sending a copy of the direction and the notice (including a copy of a map defining the area).

If it is considered that an article 4 direction is inappropriately applied, the secretary of state can make a direction cancelling or modifying the direction at any time before or after its confirmation.

Case studies

Article 4 directions have been used by a number of local authorities in England, to protect core parts of their town centres from class MA developments, with the greatest use of them being seen in London and the South East. For instance since 2022, the Secretary of State has issued modifications to 22 article 4 directions removing the PDR for changes of use from class E to class MA. Of these 13 were for London boroughs, four were for authorities in Hertfordshire and five were for other authorities in the South East and East Anglia.

In most cases the modifications related to changes to the areas covered, to reduce their extent.

However, the use of article 4 directions is only relevant where there is a significant risk of changes of use occurring. This is likely to be in areas where residential demand and prices are highest and where the centre is made up of individual units, often in separate ownerships. Where a shopping centre is in a single ownership, piecemeal redevelopment or changes are less likely to be considered.

Case studies where article 4 directions have been introduced include Camden in London and North Hertfordshire.

Camden

In Camden article 4 directions have been used to remove the permitted development right (class MA) to nearly 1,000 shops, services and clusters of employment use in the central activities zone and knowledge quarter and around 700 premises in the north of the borough.

The council originally made two article 4 directions to withdraw the class MA permitted development right to change from use class E (commercial, business, and service) to use class C3 (dwelling houses) for:

- the whole of the Camden central activities zone and parts of the Camden knowledge quarter

- sites within the north of the London Borough of Camden

Both directions came into force in July 2022 but in February 2023 the secretary of state modified them, as it was considered that a sufficiently targeted approach had not been adopted and the direction did not apply to the smallest geographical area possible. The secretary of state therefore amended the boundaries.

A separate article 4 Direction requires any change of use from launderette to residential to be the subject to a planning application at seven locations within the borough.

North Hertfordshire

In North Hertfordshire article 4 directions have been introduced for the four town centres in the area, namely Baldock, Hitchin, Letchworth Garden City and Royston. The rationale for this was to protect the vitality and viability of these areas as economic hubs, prior to the development of town centre strategies for each.

The article 4 direction was justified on the basis that the local plan identified sufficient sites to ensure the district’s housing needs are met in full and there was no specific need to rely upon any additional housing from use class E conversions which would result in the loss of class E floorspace.

In contrast the local plan identifies a need for an additional 4,500 sqm of retail, commercial and leisure floorspace in the district over the period to 2031. The article 4 directions therefore seek to ensure a suitable balance between housing and employment uses, prior to the development of the necessary town centre strategies.

In terms of the extent of the areas covered, the approach adopted by the council was to identify individual premises within the town centre and within the defined primary and secondary frontages. However, the majority of buildings in Hitchin, Baldock and Royston town centres were excluded as they are listed and permitted development rights do not apply to these properties.

In Letchworth Garden City occupiers of unlisted buildings would require consent from the Letchworth Heritage Foundations (as the freeholder for all units in the town centre) to convert a class E unit to residential use. However, the council decided for consistency and continuity to apply an article 4 direction to the non-listed buildings within the town’s primary and secondary shopping frontage as well.

The article 4 direction were made on the 5 October 2022 and confirmed on 13 February 2023. However, the extent of the areas has been questioned by the secretary of state. The council has submitted additional material to justify their inclusion of secondary frontages and a decision is awaited.

Other central government policy changes

Other recent policy changes introduced by central government include measures within the Levelling Up and Regeneration Act 2023 and mayoral development corporations. These are considered below.

Levelling Up And Regeneration Act 2023 - local rent auctions

The Levelling-up and Regeneration Act 2023 became law in October 2023 and is intended to "speed up the planning system, hold developers to account, cut bureaucracy, and encourage more councils to put in place plans to enable the building of new homes".

Many of the measures set out in the Act are not fully detailed and further regulations are required before they can take effect. As a result, the details as to how some of the proposals will work in practice will not be clear until the necessary secondary legislation is put in place.

However, important for those councils developing strategies for high streets and town centres, part 10 of the Act gives local authorities powers to bring vacant town centre properties in third party ownership into use through rental auctions and the necessary secondary legislation was laid before Parliament on 11 November 2024 and will come into force on 2 December.

The legislation seeks to address concerns that some of the vacant units being seen in our town centres result from the inaction of the landlords and a reluctance to engage with less traditional potential occupiers. As a result, community groups or businesses looking for short-term space can find letting a unit is difficult, despite high levels of vacancy on the high street.

The legislation allows councils to step in and auction vacant premises subject to the detailed requirements of the Levelling Up Act and The Local Authorities (Rental Auctions) (England) and Town and Country Planning (General Permitted Development) (Amendment) Regulations 2024.

These include:

-

a requirement for a street or area to be designated as a "high street" or “town centre” by the local authority

-

the vacant premises meeting two conditions before the local authority can proceed:

- vacancy condition – this is satisfied if on a given day the premises are vacant and have been vacant for the previous year or vacant for 366 days of the previous two years; and

- local benefit condition – this is satisfied if the local authority considers occupation of the premises for a suitable high-street use would be beneficial to the local economy, society or environment.

If these criteria are satisfied a local authority can hold a rental auction to lease the property for a set period and for a specific high street use, subject to following the detailed requirements of the 2024 regulations. During this period the property will be considered to be a new class DB use but will revert to its former use at the end of the tenancy period.

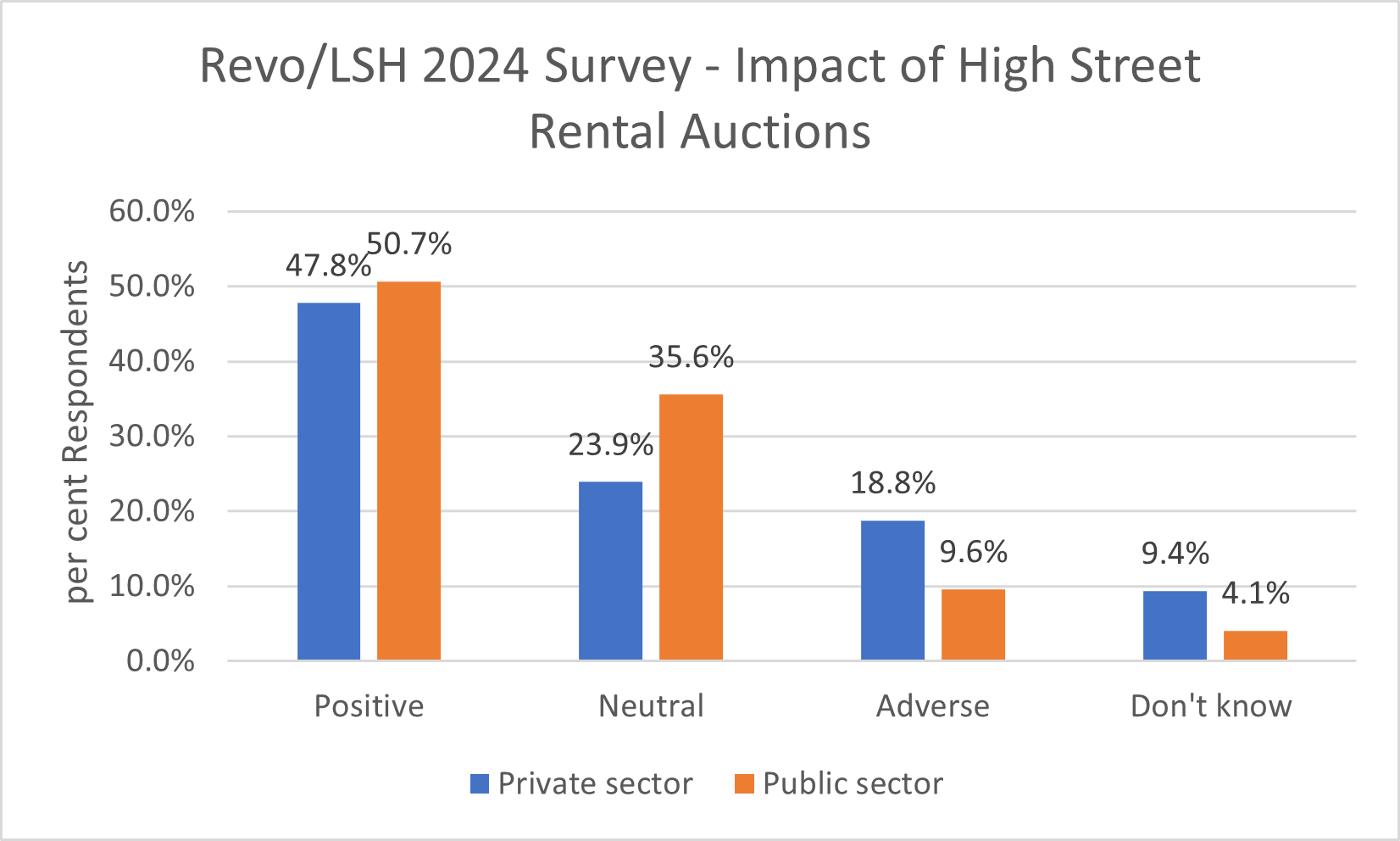

The Revo / LSH 2024 survey included a question about the potential impacts of the high street rental auctions (HSRA) and the results suggest that many respondents from both the public and private sectors consider the effect will be positive. Public sector respondents were slightly more positive about the proposal (50.7 per cent) than the private sector (47.8 per cent), while the private sector were more likely to consider the impacts would be adverse (18.8 per cent). Only 9.6 per cent of the public sector respondents were of this view.

Figure 5: Revo / LSH 2024 survey – impact of high street rental auctions

The positive support for the legislation from both the public and private sectors is likely to reflect the importance both put on the maintaining a healthy high street and bringing vacant shops units back into beneficial use. However, it remains to be seen the extent to which the introduction of these local authority powers alone may encourage the parties to work together. If not, then, as with compulsory purchase powers, it will be for the local authority to decide if they have the resources required to undertake the work and to decide if the positive benefits justify this.

The Institute of Place Management (IPM) has undertaken a consultation with experienced practitioners in the field to look at the possible impact of HSRAs. They conclude that even in places that are proactive on vacancy, HSRAs might be used against barriers to re-letting for only on or two in every 20 vacant units. There is a range of other ways to help tackle vacancy that could work before this step is needed.

IPM also notes that not all local authorities are proactively working to tackle vacancy. This may make it difficult to identify qualifying properties. The availability of sufficient skilled personnel is also raised. Instead IPM suggests other possible approaches to developing strategies to address vacancy in a meaningful and sustained way. This includes developing local intelligence and a partnership approach.

Other suggestions include:

- establishing a register of vacancy

- developing agent and landlord forums

- using a place vision/strategy to identify potential occupiers for vacant units that will strengthen the offer.

Case studies

Bristol

Bristol City Council is one area using other methods to reduce vacancy rates.

The council’s area includes 47 high streets and centres, including the city centre, 10 town, 9 district and 27 local centres. Various initiatives are being brought forward to support these centres, assisted by £4.7 million of central government funding.

One of the initiatives, the vacant commercial property grant seeks to address the same issue as the HSRA proposals, namely bringing vacant commercial units in town centres back into economic use.

The initiative has allocated £1.2 million to support small businesses, sole traders, charities, community interest companies (CICs) and arts and culture groups who want to bring a vacant commercial property back into permanent or temporary use. Funding of between £2,500 and £10,000 is available for each project.

The initiative is proving popular, with over 500 enquiries received and 120 grants approved. This confirms that there is considerable demand from prospective tenants to occupy currently vacant units. The council will be assessing the benefits of the re-occupation of the units through business rate income, business organisations and jobs supported.

However, the current funding is finite, and it is unclear whether, once it comes to an end, the HRSAs would be able to perform in a similar way. Potential concerns relate to the requirement to designate a high street or town centre and whether the local authority will have the capacity to undertake the necessary process.

Mayoral development corporations

Development corporations are public/private organisations established by government for the purpose of the development and regeneration of a specific geographic area. Historically they were initiated by central government, with the London Docklands Development Corporation established in the 1980s leading to the transformation of the area that became Canary Wharf.

Directly elected mayors in England and Wales were introduced by the Local Government Act 2000.The 2011 Localism Act introduced new legislation that allowed mayors to create their own mayoral development corporations (MDC) but it is only since the establishment of directly elected mayors outside of London that the associated powers, including the ability to compulsorily purchase property, build roads, take planning decisions and take control of existing public assets, has become more widely available.

Twelve areas outside of London now have metro mayors, covering over 34 per cent of the population of England or 50 per cent when the Mayor of London is included.

This will increase the potential for MDCs to be established, but at present, the number of MDCs is limited to six and only three of these relate to areas including town centres.

The first such area was set up by Greater Manchester’s mayor Andy Burnham in 2019 to drive the regeneration of Stockport town centre. The MDC brings together powers devolved to the mayor, with the strong local leadership from Stockport Council and the long term commitment of the government’s housing agency, Homes England, to deliver an ambitious vision for the future of Stockport town centre.

The first phase of development is well advanced and is its success to date is recognised in it being shortlisted for a number of awards in 2024.

More recently two town centre MDC areas have been established by Ben Houchen, the Mayor of Tees Valley to focus on the regeneration of Middlesbrough and Hartlepool town centres.

Middlesbrough’s MDC will focus on Middlehaven and the Zetland Historic Quarter while Hartlepool’s MDC will encompass Oakesway business park, retail and leisure land – including Mill House leisure centre and Middleton Grange shopping centre.

However, these projects are at a relatively early stage and as such the learnings from them are limited.

New powers for MDCs were also introduced as part of the Levelling Up and Regeneration Act 2023 to allow development corporations to purchase land at or close to existing use values, rather than at the much higher ‘hope’ values authorities must pay when using compulsory purchase powers. This lower price would allow MDCs to buy and prepare land for development by providing remediation, improvements or infrastructure that can be funded from the development and planning gain.

These powers are still untested but theoretically councils could take control of their high streets by setting out a vision and plan, setting up a development corporation to fund and deliver that vision in terms of transport and social infrastructure to support housing. A recent report from the Bennett Institute at the University of Cambridge sets out how such development corporations using changes in the Levelling Up and Regeneration Act 2023 could work.

Future initiatives

The final consideration in this report is what other changes may be made by central government that will impact on local high streets and town centre strategies.

The new government has made clear its continued support for a plan-led approach to development and the proposed changes to the NPPF would strengthen the role of plans further. The Labour Party’s 2024 general election manifesto also called for every area to develop a Local Growth Plan, bringing together spatial, transport, energy and skills plans alongside other areas to drive growth.

The new government has also indicated its support for town centres and high streets and the early actions in relation to proposed changes to the NPPF suggest that the overall approach will be to maintain existing policy, supporting town centres and taking a positive approach to their growth, with no changes to the policy wording proposed at the present time.

Budget October 2024

The October 2024 budget also indicated the government’s support for the high street and small businesses, confirming funding for MHCLG’s core Levelling Up Fund projects and providing £1 billion in 2025‑26 to revitalise high streets, town centres and communities.

Permanent changes to business rates were also proposed, with the specific objective of protecting the high street by assisting smaller retail, hospitality and leisure businesses (RHL). This includes introducing permanently lower multipliers for lower rateable value RHL properties (under £500,000) from 2026/27, paid for by a higher multiplier for properties with rateable values above £500,000.

A discussion paper has also been published setting out potential areas of business rates reform, and the Budget also included the extension of temporary support for the RHL sector through rates relief, albeit at a lower level than previously.

However, at the same time changes to employee national insurance contributions and the national living wage will increase businesses costs.

Brownfield passports

A recent MHCLG consultation working paper on potential brownfield planning passports may provide the clearest indication of the Government’s current thinking on future planning reforms. The working paper emphasises that brownfield land should be the first option for new development and supports the better use of existing land and buildings, especially where intensification supports local centres. To support this the working paper suggests the introduction of “brownfield” passport where the acceptable form for development is set out, and compliant proposals can be quickly approved. The wider use of local development orders to grant area-wide permissions is also proposed.

This approach would be relevant to all new development and existing developed land, not just town centres, but is important in that it is supporting a streamlined approach to planning but one which continues to rely on a ‘plan-led’ approach.

Summary and conclusions

Summary

Our town centres and high streets have, in the main, developed over centuries of organic growth, adapting to changing circumstances and customer demands without the need for central or local government intervention.

Traditionally they have been centres for a range of activities but the period of growth in disposable income and technological changes in the late twentieth centre led to the rapid expansion of the retail offer, with the result that town centre economies became synonymous with shopping.

More recently structural changes in the retail sector and the way customers shop has seen a decline in the demand for retail floorspace and the need to diversify the town centre offer has been recognised. However, the Covid-19 pandemic, the cost of living and energy crisis and on-going changes in consumer behaviour has exacerbated the problems faced and it is accepted that most centres now have more retail space than they require.

The response from both central and local government has been to become more involved in the planning of our town centres, bringing forward initiatives to assist in their adaption to the new and challenging climate in which they operate.

At a local level this includes adopting appropriate planning policies to support town centres and the development of long-term visions and strategies.

At a national level, central government has also become involved, providing additional funding streams for selected town centres and introducing changes to national planning policy aimed at helping town centres adapt quickly to the changing circumstances.

The introduction of policy changes at national level however, has the potential to affect policies and strategies that have been developed locally. The introduction of a broader use class covering many town centre uses (class E) not just retail, had the effect of rendering any local policies seeking to control the proportion of non-retail space in a core shopping area, obsolete.

Similarly, the introduction of permitted development rights to allow the conversion of class E properties to residential use (class MA) has the potential to harm the continued provision of active frontages.

However, these changes also provide important positive benefits for the planning of town centres, allowing occupiers and landlords to respond in a timely manner to changing market needs and allowing the reoccupation of currently vacant premises.

The introduction of new powers to allow local authorities to hold high street rental auctions of vacant properties could also be positive in increasing occupation and the range of offer provided.

Conclusions

The introduction of changes at national level however can create difficulties for the local authorities with responsibility for maintaining and enhancing town centres, as every town centre and high street is unique. They have different histories and serve different communities with different needs and requirements. As a result, national policies can never be fully appropriate for a specific location.

The changes being introduced generally reduce the controls councils have at their disposal to stop things happening. However, best practice has shown that the key to a successful high street strategy is positive engagement, encouraging all those with a stake in a centre to work towards a common vision. The key to successful town centres is therefore the development of clear local policies and strategies that can attract in investment and the desired uses.

Best practice has shown that these strategies need to be well articulated and supported locally, but it is also essential that they reflect the economic and social realities they operate in. They also need to be flexible to adapt to the unforeseen changes that will inevitably arise during any plan period.

In this context, changes to use classes or permitted development rights may have a short-term effect locally, but these changes are simply one reaction to the underlying changes already being experienced – the decline in demand for retail space means a wider range of uses needs to be provided in town centres if beneficial uses are to be found for existing units and pressure to increase residential provision will arise if needs are not being met elsewhere.

These policy changes therefore do not negate the need for local high street strategies but instead should be seen as one of the changing factors which a successful strategy needs to adapt to. Successful town centres are those with a long-term vision that reflects the needs of and has the support of the local community, including the private sector. Local authorities need to lead in developing this the vision for their high streets and this vision must be clear and evidence based, in a policy environment in which central governments are pushing for greater permitted development, whether through the adaptation of the use classes or redevelopment on brownfield land.