Executive summary

This is the fourth review of the Local Government Association (LGA) Strategic Market: Insight and Relationship Programme (formerly called the Strategic Supplier Relationship Management (SSRM) Programme). The LGA’s National Advisory Group (NAG) for Procurement commissioned the programme in 2019 to improve dialogue with strategic suppliers to local government; up to that time local government had not always acted strategically across councils in its view of supplier markets and the companies that operate within them, and a key aim of the programme has been and remains to rectify that position.

The SSRM programme achieved several successes and was relaunched at the beginning of 2024 with an additional focus to provide awareness and understanding of the operation of the key markets that local government engages with.

The overall spend by local government on third parties in 2024/25 was around £100bn. In the five years of operation the programme has been successful in providing councils with market intelligence and a better understanding of the impact (and sometimes frustrations) that councils have with their strategic suppliers to seek to improve the effectiveness of that spend. This is making local government think differently about how it needs to interact with markets.

Overview

About the LGA

The LGA is the national membership body for local authorities and works on behalf of member councils to support, promote and improve local government.

The core membership of the LGA comprises 315 of the 317 councils in England and includes district, county, metropolitan and unitary authorities along with London boroughs and the City of London Corporation. The 22 Welsh unitary councils are in membership via the Welsh Local Government Association.

The LGA also operates an Associate arrangement for those organisations whose purpose and objectives are aligned - Associates include fire and rescue authorities, police, fire and crime commissioners/police and crime commissioners, national park authorities and town and parish councils via the National Association of Local Councils (NALC)’s corporate associate membership.

The LGA is a politically led, cross-party organisation that works on behalf of councils to ensure local government has a strong, credible voice with national government. The LGA aims to influence and set the political agenda on the issues that matter to councils, so they can deliver local solutions to national problems.

The LGA provides a range of practical support on a free of charge and/or subsidised basis, to enable local authorities to exploit the opportunities that this approach to improvement provides. This includes support of a corporate nature such as leadership programmes, peer challenge, LG Inform (our benchmarking service), and programmes tailored to specific service areas such as children's, adults, health, care, financial, culture, tourism, sport and planning services.

National Procurement Strategy (NPS) for Local Government

The LGA’s NPS for Local Government was last refreshed in 2022. The NPS focuses on three key priorities for the local government procurement sector:

- Showing leadership. This includes information on engaging with senior managers, councillors, strategic suppliers and partners in relation to procurement and commercial matters and why this is important.

- Behaving commercially. This focuses on the importance of creating commercial opportunities and income generation, managing risk and managing existing contracts and relationships.

- Achieving community benefits. This deals with creating social value through procurement, engaging with SMEs and micro businesses and engaging with voluntary, community and social enterprise (VCSE) groups. The NPS also outlines the key ‘enablers’ which will assist local authorities in meeting these priorities. These include adding value, developing talent, exploiting digital technology, enabling innovation and embedding change.

Strategic Market: Insight & Relationship Programme (SMIRP)

The SMIRP is a continuation of the LGA’s SSRM programme which engaged with identified ‘strategic’ suppliers to local government (based initially on spend) to form a fundamentally different relationship with them. The programme achieved many successes and following a pause owing to budgetary issues was relaunched with an additional focus to provide awareness and understanding of the operation of the key markets that local government engages with.

The revised objectives for the programme are set out below.

Strategic objectives

- Provide councils with an awareness and understanding of the operation of key markets with an aim of identifying potential market or strategic supplier failure.

- Act, in a similar way to the ‘Crown Representative’ for markets such as Adults and Children’s services.

- Provide a focus on the Construction and ICT markets and maintain a watching brief on other key markets.

- Act as a useful point of contact for questions on strategic suppliers, markets or matters of urgency relating to local government procurement.

- Facilitate best practice for sharing quality procurement data by working with central government on the single platform to enable the central gathering of data to be shared locally.

Operational objectives

- Form a fundamentally different relationship with suppliers and markets that will focus on their ability to be innovative, add value and be transparent across the whole of local government rather than individual contracts.

- Encourage supply chain innovation, by looking at ways to reduce costs, increase insight, and develop better, more strategic relationships.

- Convene groups of councils and experts in the event of incidents with significant impact such as supplier or market failure or cyber-attack.

- Gather and share examples of best practice in commissioning and procurement e.g. by identifying ways in which councils can work with markets to become carbon neutral and to showcase success in using the new Procurement Act 2023 ‘Competitive Flexible Procedure’ to drive innovation.

Local Government Third Party Spend

Reported third party spend shows that local councils spent around £91bn during 2024/25 which, together with tail spend below £500 (that councils are not required to report on) gives an estimated figure nearer to £100bn.

During the year the SMIRP has worked to monitor and engage with key local government suppliers and providers across multiple sectors and markets. These are:

- adults

- children’s services

- construction

- ICT (includes liaising and supporting digital, artificial intelligence and cyber security).

The total spend across these four category areas is £44.11bn meaning that the programme is actively reviewing 47 per cent of the total local government spend.

The programme is also participating in work to ensure that local government will have access to any data analysis from the Government’s Central Digital Platform, also known as the Find a Tender Service.

This report sets out progress during 2024/25 in determining the key issues affecting these markets.

Strategic Market: Adult Social Care (ASC)

Strategic Market leads: Gail Stephens and Greg Povey

Overview of expenditure

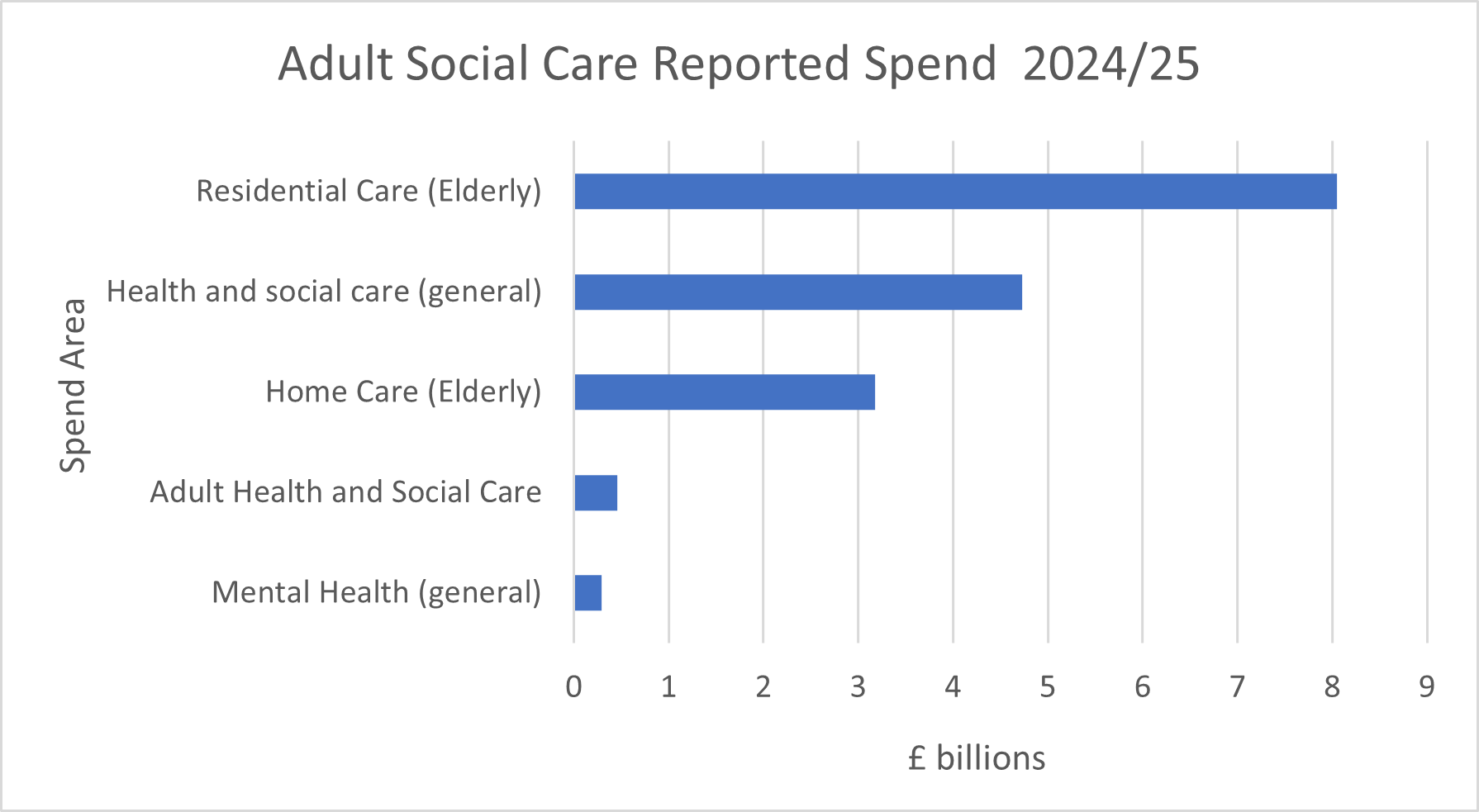

Councils reported spending approximately £16.71 billion on ASC during the 2024/25 financial year.

Overview of the year

The year started with a review of the scope of the strategic market which had previously focussed largely on nursing homes; a new format was designed and the focus broadened to include the whole Adult Social Care (ASC) market. Resulting from this the strategic market leads developed relationships with key suppliers across a wider range of ASC markets.

Meetings were held with strategic suppliers on a regular basis using the new format which included presentations by key representatives, an introduction to the background of the provider, a discussion on the organisation’s strategic direction of travel for the next three years and the key challenges and opportunities foreseen.

The aim of these insights was to help procurement officers in the ‘Plan and Define’ stages of procurement and commissioners in the ‘Analyse, Plan and Review’ stages of commissioning who may wish to learn about best practice and issues specific to the subcategory before going out to tender.

Recognising that the Procurement Act 2023 (PA23) would go live during the financial year, each meeting provided an update on Cabinet Office’s Transforming Public Procurement (TPP) workstream, discussed the learning and development offer and information released in that quarter. Topics covered included the new National Procurement Policy Statement (NPPS) and the Central Digital Platform (CDP).

A particular issue raised that required further clarity concern the changes to the Light Touch flexibilities as practitioners were familiar with the principles under the Public Contract Regulations 2015 but were uncertain how the changes would operate following introduction of PA23.

The queries from network members and example business uses are the subject of discussions with Cabinet Office to review if there is a need for further guidance as they are keen to make sure the guidance on Light Touch is clear.

The following section explores the topics raised by providers in more detail by theme:

Politics

The providers considered that their landscape is characterised by political change and uncertainty as the policy actions of the new Government were noted. Their initial areas of focus on were the NHS, commitments to worker’s rights, changes to national insurance contributions, reforms to disability benefits and universal credit; all whilst the promised social care reforms started by the previous Government are either overdue or abandoned (cost of care).

Economics

The backdrop for the year was that the UK economy showed signs of mixed performance, facing challenges such as sluggish growth, concerns about rising inflation and the impact of upcoming tax increases on businesses. On 15th May 2025 the Office for National Statistics (ONS) published the "Economic activity and social change in the UK, real-time indicators which showed that “Real GDP per head is estimated to have grown by 0.5 per cent in Quarter 1 2025, following two consecutive quarterly falls.” It is perhaps unsurprising this was the number one issue raised by suppliers who highlighted the following issues:

- The increase

- National Living Wage uplifts out stripping uplifts by councils

- Gap between cost of care and council rates for care increasing

- Council’s uplift processes

- The ability of commissioners to support innovation with adequate funding

- Facing new pressures due to recent national insurance contributions changes adding to costs

- Some providers making losses over several years leading, in some instances, to services being handed back to councils driven by a combination of factors including local labour market, geography, future growth prospects, commissioner/provider relationship, quality of property, councils’ rates for care, and the lack economies of scale.

- Affordability of services for residents

- Fundraising to support operations of charities and VCSEs.

- Some providers have a historic lack of investment in property or technology

Housing

The availability of housing supply for adult social care service users was frequently raised. Other related issues noted were:

- High construction inflation costs mean only developments that are viable and are higher end ‘all for sale’ developments are being completed. Shared ownership is getting squeezed out and social rent is disappearing.

- Cost of development following construction inflation and fire/building safety costs is presenting challenges

- In some cases, alternative financing models may be needed to support development.

- Leasehold reform and cost causing some providers to pause development activity

- Planning requirements for developments

- Voids/property reprovision

- An unstable property market

- A trend of hospitality sector influenced design of residential services

- Whether councils could consider framing land or capital contribution under the Subsidy Control Act.

Demand

Providers are noting residents coming to them with higher frailty and increased care requirements as they feel the impact of increasing health needs from an ageing population.

Commissioning

Providers are keen to have conversations with commissioners about growth in a proactive manner, collaborating early, to talk as partners about future provision with an aim to establishing long term partnership agreements for care services.

Providers want to plan in unison and start earlier engagement on key needs such as the ageing population, hospital discharge, and the transition of children into adult services.

Providers used research to try and improve the lives of residents as key, as well as the sector tackling inconsistency in commissioning processes.

Service design

Service design was mentioned by many providers as a key theme, at the heart of this was modernising services to ensure relevance for the next generation, and often this was tailored to the markets they focus on:

- moving from providing homes for life to supporting people to thrive in their homes and their communities

- creating inclusive models of housing, employment and community involvement

- advocacy to improve the quality of life of people

- the lack of a blueprint of what good social care looks like for working-age adults.

Providers want to partner with other providers to create services as well as partner with other agencies (for example NHS, other older people charities, universities) to deliver services.

Staffing

The widely publicised issue of staff shortages in the sector was highlighted by every provider mentioning that recruiting, developing and retaining talented people was key especially given the supply of skilled labour.

Regulations

Increasing regulatory requirements and changes, together with legislative changes are felt to be placing increasing (disproportionate) demands on smaller providers.

The effectiveness, performance and behaviour of the regulator was constructively challenged, and the question posed, “Has it been a driver for excellence?”

The changing landscape for leasehold properties and impact on social care schemes such as Extra Care was highlighted.

Other issues

- Providers are keen for councils to maximise the use of flexible procurement approaches provided under the Procurement Act 2023. Some wish the use of frameworks to be maximised to reduce bidding and administration costs and reduce the diversity of practise and purchasing behaviour employed by councils.

- Providers see making the use of technology as both an opportunity and a challenge. The technology most likely to be adopted will be AI to automate administrative tasks and reduce back-office costs whilst joining up data and systems to deliver better outcomes.

- Whilst the net zero agenda was mentioned this was not widely a focus of provider feedback, perhaps unsurprising as they focus on issues considered more pressing in the short term.

Key achievements

The new format for engaging with strategic suppliers has proved very engaging with procurement and commissioning officers as the number attending or expressing an interest in the network grew from 32 in 2023/24 to 71 in 2024/25, a 122 per cent increase.

Each quarter a subcategory of the overall adult social care category area was put under focus, voted for by members of the network. To date subcategories that have been put under focus have been:

- Supported Living for Adults with Learning Disabilities, Mental Health and Autism supported by Lifeways, Leonard Cheshire and Mencap.

- Extra Care/Supported Housing subcategory supported by the Housing LIN a dynamic community of over 15,000 housing, health and social care professionals in England, Wales and Scotland, Housing 21, and The Extra Care Charitable Trust.

The identification of key suppliers to invite and participate in a subcategory focus is made through an analysis of the spend data for the subcategory available to the LGA from Insights; the Find a Tender service and a poll of network members to see if there were any particular providers they were keen to hear present.

The meetings with the strategic providers highlighted that need is increasing, funding is not keeping pace and, in a sector where great people are needed to deliver great support, talent is increasingly hard to find and retain.

Proposed activities for 2025/26

It is intended to undertake the following activities during 2025/26:

- continue ongoing engagement and dialogue with local government representatives from the strategic adult social care providers

- continue to observe and report on strategic changes within the sector and the impact of any new reforms (such as NHS England, ICB reorganisation and Local Government Reorganisation) or market changes.

Strategic Market: Children’s Services

Strategic Market leads: Becky Polito and Karen Faulkner

Overview of expenditure

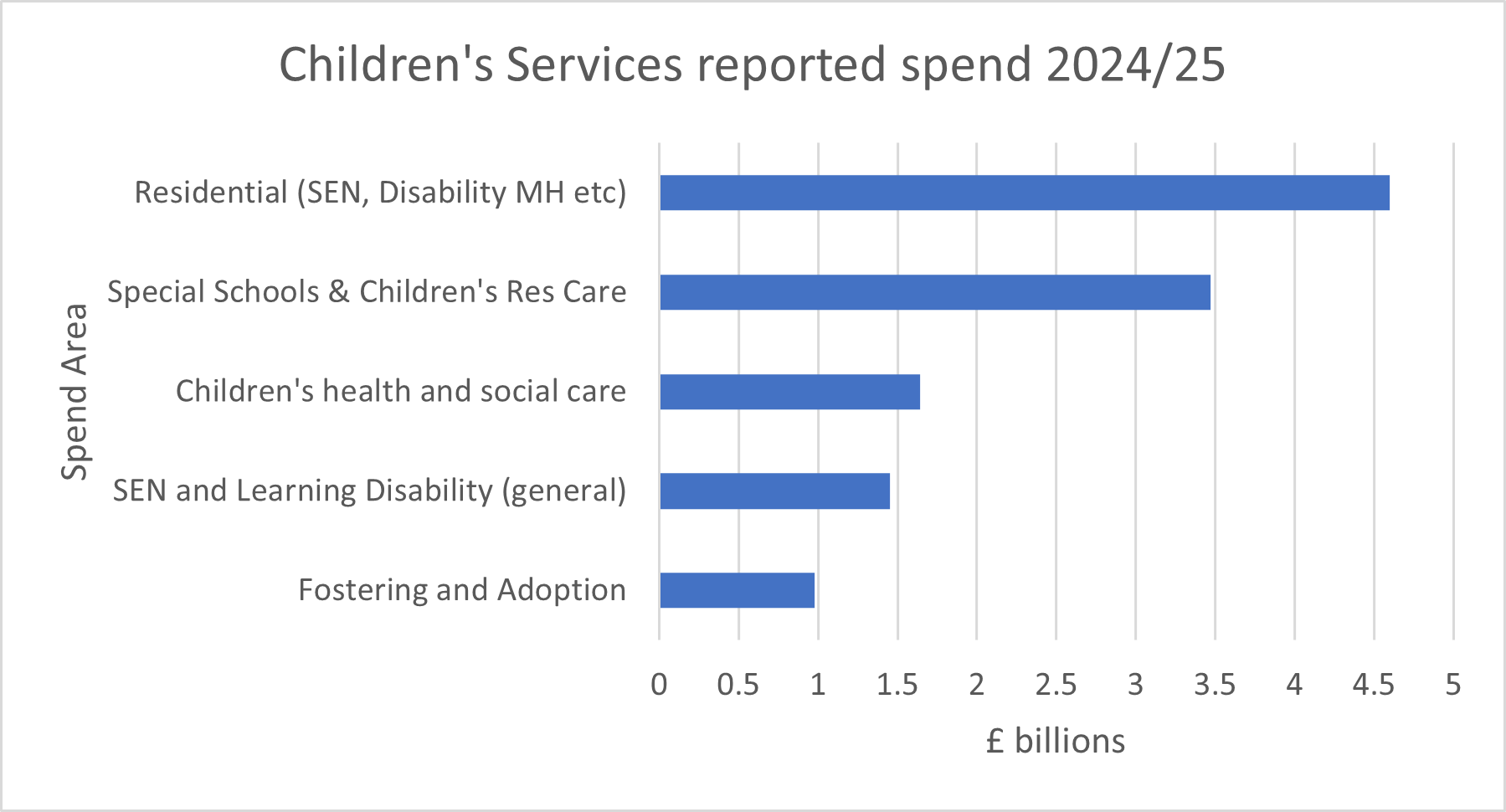

Councils reported spending approximately £12.14 billion on children services during the 2024/25 financial year.

Overview of the year

There have been several areas across the sector that have been the focus of discussion in 2024/25, these include, but are not limited to:

- The embedding of regulation for post-16 Supported Accommodation services:

- The Supported Accommodation (England) Regulations 2023, with mandatory registration with Ofsted became effective on October 28, 2023.

- Rising costs of placements for Children and Young People with complex needs:

- The cost of placing children with complex needs in residential care is rising significantly, driven by factors such as increased demand, higher complexity, and escalating fees for private providers.

- Residential placements have seen dramatic increases, with some costing over £10,000 per week, and the number of such high-cost placements has soared. The challenges are explored more fully in the National Children’s Bureau (NCB) report Costs and complexity in care.

- The Government’s position on the future of Regional Care Cooperatives (RCCs):

- The UK Government is actively promoting the implementation of RCCs within the children’s social care system. They are piloting RCCs in two areas with the aim of rolling them out England-wide after evaluating their effectiveness, potentially as early as October 2026.

- Preparation for and commencement of the Procurement Act 2023:

- The Procurement Act 2023 came into force on 24February 2025. This date marked the beginning of the new procurement rules, which aim to improve and streamline how public bodies buy goods and services. The Act applies to all procurements commenced on or after this date, including Children’s Services.

An action plan for the year was compiled following exploratory conversations with the following organisations - Nationwide Association of Fostering Providers (NAFP), Department for Education (DfE), National Association of Supported Accommodation Partners (NASP), Supported Accommodation Association, Scotland Excel, and Ofsted.

The action plan focused on work under the SMIRP Operational Objectives.

Key achievements

The SMIRP leads undertook the following activities during the year:

- Met with a range of membership bodies and Ofsted to identify priorities to ensure these were incorporated into the action plan. Follow up meetings were held to progress agreed outcomes.

- Engaged with NAFP to understand common complaints from independent foster care providers, and to identify if there are any themes for councils to address. The quality of referrals continues to be of concern, and some work is taking place within councils across the country to improve quality.

- Worked with Ofsted to promote their webinars on “Children’s homes and health care: understanding registration requirements for Ofsted & CQC” which took place in November 2024. The information shared at the event can be found here Children’s homes and health care: registration with Ofsted or CQC – GOV.UK

- Created a national Children’s Cross Regional Arrangements Group (CCRAG) Market Analysis Tool that provides valuable insight into the private and councils markets from July 2020 – July 2024. The tool analyses the numbers of providers entering/leaving the market, change in the number of settings and inspection ratings. The tool has been used to support the development of local sufficiency strategies.

- Met with Scotland Excel to begin exploring the how the children’s social care markets work in Scotland and how this impacts markets in England and Wales.

- Successfully worked with Placements in Northwest, West Midlands, and White Rose Consortia to promote the Local Placement Alert Function to support placement finding to children and young people locally where possible and appropriate.

Key Outcomes

The following outcomes were achieved during the year:

- increased national awareness of the SMIRP programme

- increased efficiency in the use of Ofsted generated data available to councils

- increased understanding of the issues facing the supported accommodation sector and the impact regulation is having on the sector.

Proposed activities for 2025/26

- Establish systems that can act as a single point of reference for best practice in the sector.

- Further explore the correlation between the Scottish and English and Welsh markets and how these can be of benefit to councils and providers.

- Make connections with new staff in Ofsted to support the flow of information between Ofsted and councils.

- Following on from the recommendations in the NCB report on ’Costs and complexity in care’ continue to look at ways to foster stronger relationships between council’s and providers, encouraging open communication channels and mutual respect.

Strategic Market: Construction and Infrastructure

Strategic Market lead: Bev Thomas

Overview of expenditure

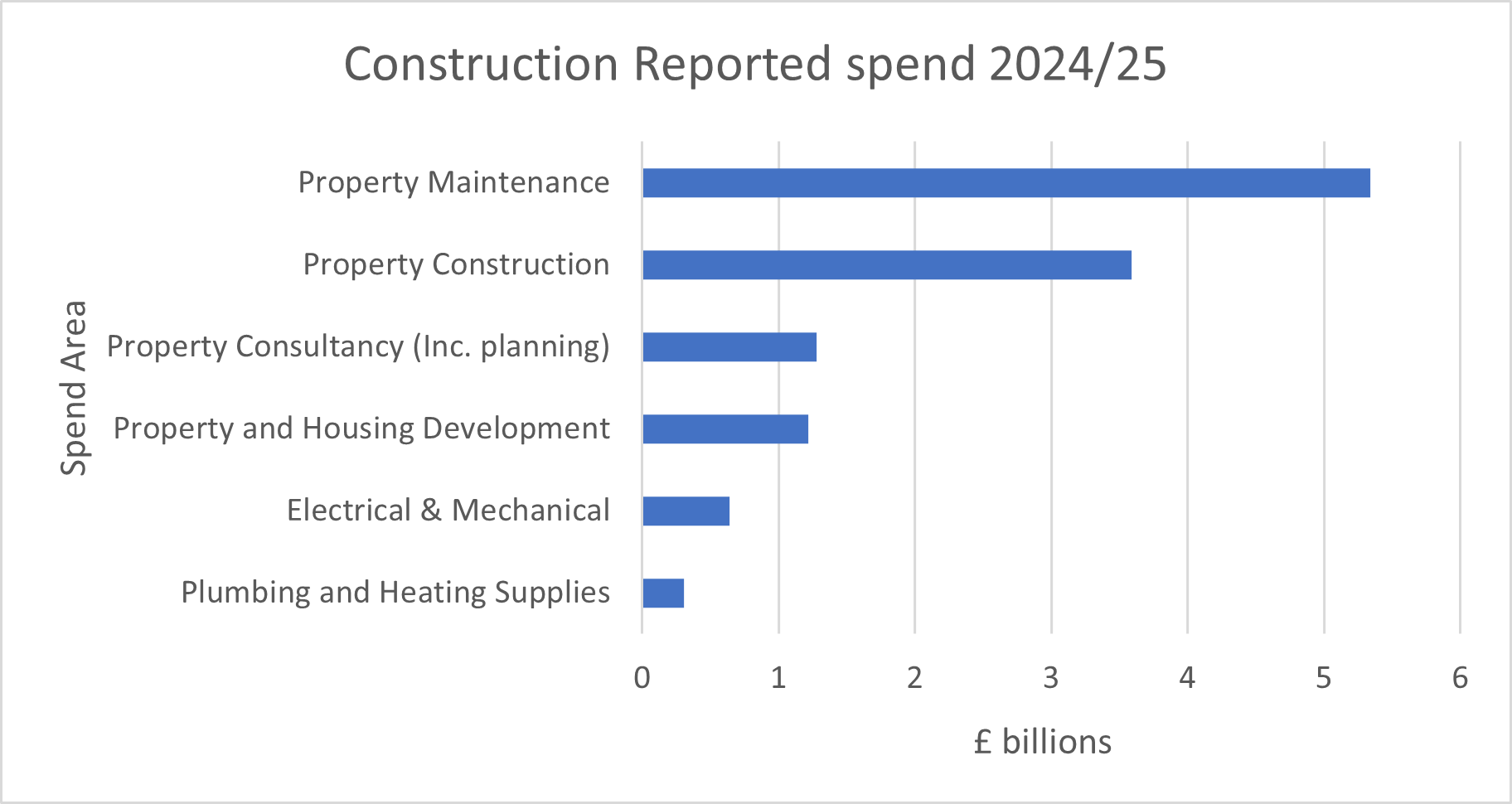

Councils reported spending approximately £12.4 billion in this market during the 2024/25 financial year.

Overview of the year

There have been many challenges facing the construction industry in recent times such as the changes required following the Grenfell tragedy, the UK leaving the European Union and the COVID-19 pandemic. Councils have shown their ability to adapt and address these issues.

Local government also spends around £9.14 billion per year on buildings and capital projects not related to construction such as the acquisition of land and existing buildings, and the running costs of premises. It is important that these contracts are procured more efficiently to deliver value for money, add social value and reflect the requirements of the Procurement Act 2023.

Market insight was also obtained by examining data the following sources:

- The Office of National Statistics (ONS) bulletins on the Construction output in Great Britain provides a monthly overview of estimated growth in construction, where the increase came from ie new work, repair and maintenance and the sectors that had growth in the month.

- National Association Construction Frameworks – NCAF: Market Intelligence Reports – the reports are quarterly and provide an overview on what is impacting the sector such as Ukraine conflict, cost of living crisis and building costs increase.

The key issues facing the sector includes inflationary pressures, the labour market – shortage of skills workers and regulatory pressures such as the Building Safety Act 2022.

Key achievements

The key activities undertaken during the year are set out below.

- Sought the views of the Construction Steering Group on the key areas of activities that would be of benefit and interest to them to enable an update of the National Construction Category Strategy in 2025.

- The LGA Construction Steering Group meetings were held on a quarterly basis throughout the year and attended by the SMIRP lead. Discussions points included:

- Gaining a better understanding of what is happening in the housing market, Government new home targets and Grenfell findings, including reviewing the data about the sector from sources such as Oxygen Finance and NACF on the market and future challenges etc.

- Identifying councils using the Modern Method of Construction (MMC) and promote any case studies (Council House Building Programme: Wiltshire Council | Local Government Association)

- The common assessment framework, value toolkit, carbon reduction price increases, the Building Safety Reform Bill, the Digital Working Group, the Construction Playbook and the Constructing Gold Standard Review and implications of the Procurement Act 23 and the National Procurement Policy Statement (NPPS).

- The SMIRP lead supported the planning and implementation of the LGA Annual National Construction Conference held virtual over two half-days (11 and 13 February 2025), with speakers from the wider public sector, Cabinet Office and industry experts.

- The SMIRP lead attended a meeting with the Civil Engineering Contractors Association (CECA) to hear more about the Association proposed project/ research into frameworks. It was recognised that frameworks were a good way of organising and delivering civil engineering projects. However, not all frameworks worked effectively and were a challenge for its members when seeking work through frameworks. Several themes and questions were suggested to further guide the Association research.

Proposed activities for 2025/26

- Develop a workplan that shapes, lead and communicates on national legislation, regulations and policy, including sharing expertise and good practice ie use of podcasts.

- Update the national Construction Category Strategy.

- Continue to increase the Steering Group membership

- Resume engagement with the Government’s Crown Representatives to explore issues at a local level.

- Continue to engage with industry, national and professional bodies.

- Support the preparation and delivery of a virtual/hybrid National Construction Conference Webinars in 2026.

- Act as conduit between the LGA’s National Advisory Group (NAG) for Procurement and the Construction Steering Group.

Strategic Market: Information and Communications Technology

Strategic market lead: Terry Brewer

Overview of expenditure

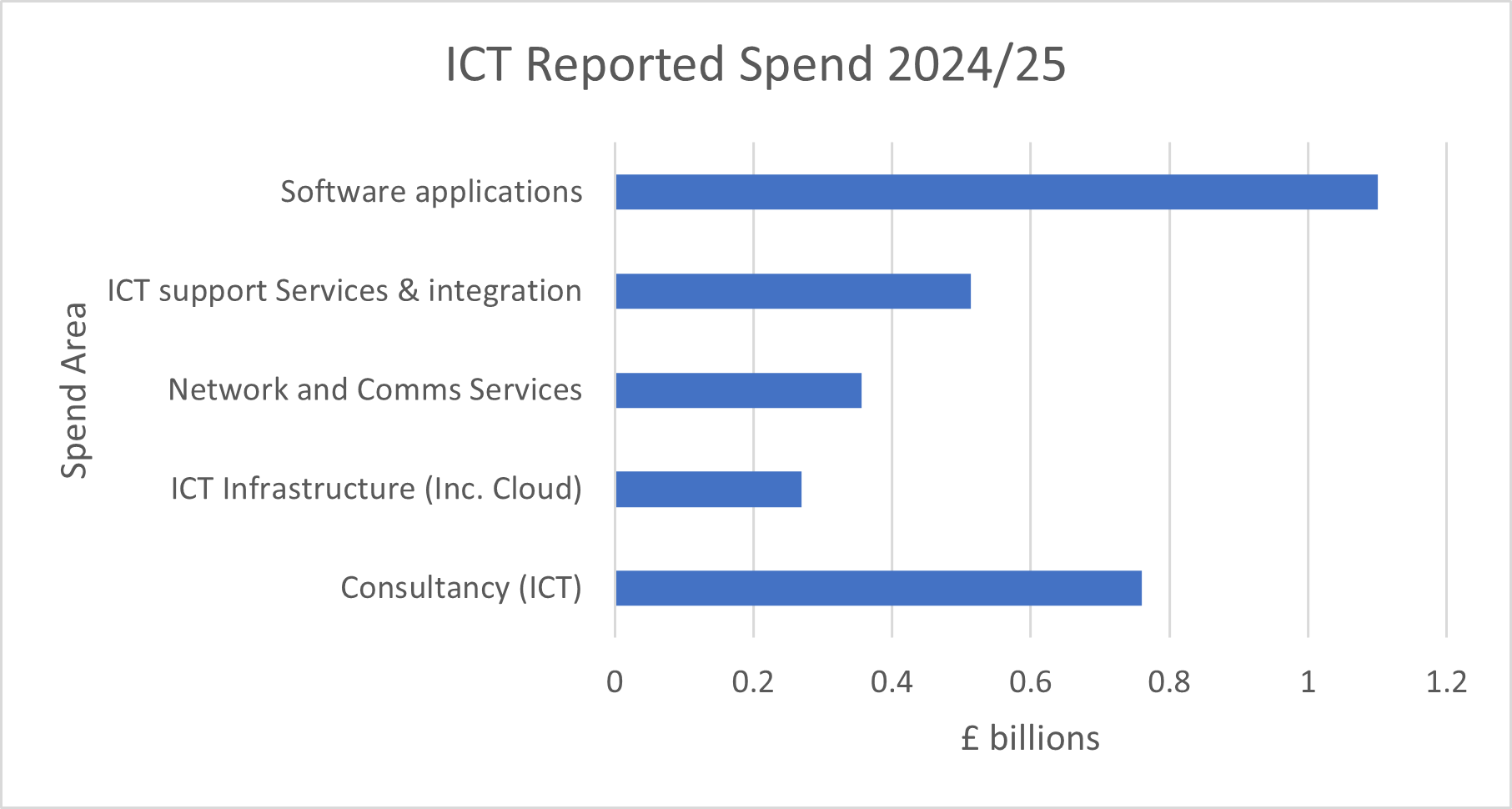

Councils reported spending approximately £2.9 billion in this market during the 2024/25 financial year.

Overview of the year

A key priority for the year has been cyber security – particularly focused on the supply chain. Following several supplier incidents impacting on councils and their residents including two impacting social care providers, a ransomware incident and a data incident, a need was identified to enable councils to better manage the risk and fulfil their data protection statutory duties. Of particular concern is that the current assurance and legislative landscape does not provide sufficient protections for councils to keep their residents safe in the context of a supplier incident.

The market lead liaised with the LGA’s Cyber, Digital and Technology team to explore ways in which councils might be assisted to manage the risk to residents and to seek to influence a change in legislation to have a more people-centred perspective in cyber incident response.

The key issues identified were:

- the need to build an understanding of the impact on local government

- address the lack of incident response plans for major supplier incidents held by lead Government departments with local government understanding

- lack of regulatory certainty under the Data Protection and Digital Information Bill

- lack of confidence in some suppliers

- resources to identify impact on residents

- contract management/clauses – important but resources limited.

The plan over time is to build on the work already taken by the LGA to improve the situation for councils, which included developing ‘embedding cyber resilience in the supply chain’, e-learning and web guides and developing a guide for Heads of Procurement.

The priority areas were to explore the development of contract clauses, a standardised assurance framework or tool for local government, to work with Department of Health & Social Care (DHSC) and Department of Education (DfE) on a supplier incident response plan owned by the lead government department, and to advocate for councils needs in strategic supplier engagements – particularly considering what the ideal terms and conditions are for councils with key suppliers.

The clauses for councils should clearly define contractors’ cyber security responsibilities and understand risk ownership and require contractors to implement accessible policies, utilise feedback mechanisms, and employ skilled professionals in security roles.

Additional training might potentially be needed to highlight that councils should avoid, where possible, letting contracts on provider terms and conditions – because a contract clause requiring them to keep a council informed if there is a cyber-attack will not be part of the contract.

Engagement with Industry and Membership Bodies

Discussions were held during the year with the two key bodies for the ICT sector, the Society of Innovation, Technology and Modernisation (SOCITM) and TechUK.

TechUK

TechUK is the trade body for the ICT industry. It has 950 companies as members around two thirds of whom are SMEs. The market lead had attended a meeting of Tech UK’s Public Sector group; at the time of the meeting the Procurement Bill was passing through Parliament, and a presentation was provided to the group on the changes to procurement that the Bill was anticipated to bring about. There are many SMEs providing digital services and there was a need to ensure they are aware of the Procurement Act 2023 and how to engage with local government. A copy of the presentation provided to TechUK on the Act was sent on to the organisation so that they could pass this on to their members.

At the meeting the key issues that companies in the ICT market experience in dealing with Local Government were identified as follows:

- procurement pipelines – it was noted that this area should greatly improve following implementation of the Procurement Act

- lack of early market engagement (especially where framework agreements are used)

- digital skills are not widespread across local government and there is a need to provide as much support as possible to assist with key issues.

- difficult for new entrants and SMEs to get a foothold with local councils

- number of members are finding Social Value a difficult issue particularly SMEs

- lack of specialist IT buyers in councils

- cyber security.

It was agreed that the actions set out below would be followed up:

- arranging a social value webinar for Tech UK members (this was delivered by SMIRP lead)

- providing a webinar for ICT leads/IT buyers in local government.

The LGA signed an MOU with TechUK on 23 April 2025 to take forward more constructive engagements between local government and key technology suppliers.

SOCITM

SOCITM is a membership organisation of more than 2,500 public sector professionals helping shape and deliver public services in the ICT area. A positive discussion was held on the key issues facing local government and how SOCITM role and resources might be able to assist to address some of the concerns identified.

Artificial Intelligence (AI)

The increasing use of artificial intelligence was a prominent issue during the year, with growing interest from councils as to how they might be able to harness the power it offers to improve services to residents and achieve efficiencies.

The LGA published a guide – Responsibly Buying AI – which is structured around the specific roles involved in the commissioning and procurement of AI within councils in England which was developed in partnership with the key regulators: Information Commissioners Office (ICO) and Equality and Human Rights Commission (EHRC) as well as the London Office for Technology and Innovation (LOTI).

The LGA also repeated its survey to explore the use of AI in English councils. The purpose was to build an updated picture of where AI is currently being deployed in local services and council business units and to map where the greatest opportunities and risks lie.

Proposed activities for 2025/26

Develop an incident response plan with the Department of Health and Social Care (DHSC) with clear roles and responsibilities for the lead Government department to provide clarity for councils when a major supplier incident occurs.

It is envisaged that DHSC will be to set the precedent for other lead Government departments given they hold he highest levels of capabilities and capacities across Government.

- Undertake a joint discovery with MHCLG on developing profiles of the top twenty strategic suppliers to local government (that do not also sell to central government) and work with councils to develop future focused terms and conditions related to suppliers and key products they offer.

- Consider how a national standardised assurance template/tool could be developed building on the work of the Scottish Government, councils in North East England and London.

- Re-engagement with Original Equipment Manufacturers and resellers who transact opportunities with local government for hardware or software.

- Follow up with TechUK and SOCITM.

- Identify how best the programme can support councils with the growing use and interest in AI.

Strategic Market Support: Procurement Data

Strategic lead: Greg Povey

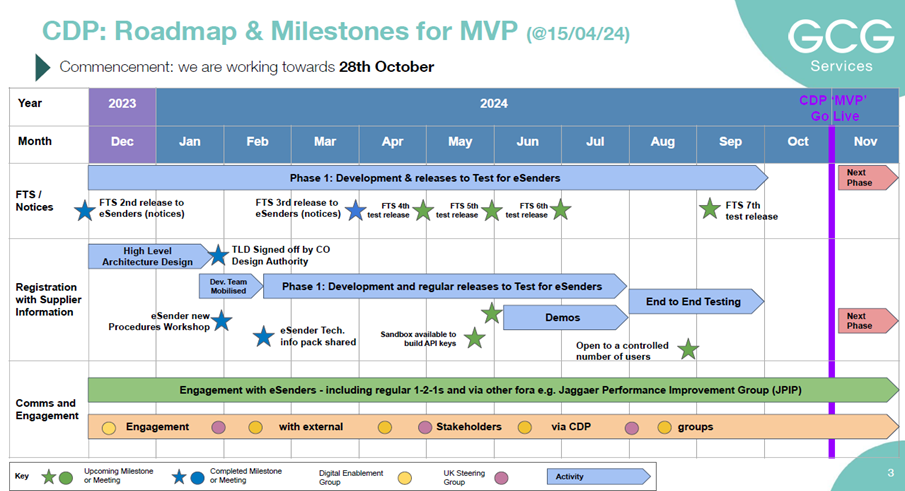

Most of the activity in the workstream during the year involved attendance at Cabinet Office UK Steering Group meetings. The meetings were focussed on the relaunching of the Find a Tender Service (FTS) as an output of the Central Digital Platform (CDP) strategy. In practice it is this group that leads on the application of the Open Contract Data Standards that all the new FTS functionality will be using, and which will hopefully enable the data analysis being sought by councils.

The focus of the steering group has been in producing the new notices and APIs required for e-senders to link with FTS and monitoring the e-senders state of readiness to be ready for go live.

The steering group has been clear that development of the CDP will be in phases (see image below), with phase 1 covering all aspects required to issue tenders, phase 2 around performance and modification notices and a potential phase 3 to develop several tools.

Proposed activities for 2025/26

- Continue to seek to enable local government’s access to data analysis tools via the CDP.

- Continue to engage with the Cabinet Office Data & Analytical Services Team to identify which team is working on data tools and to follow up as appropriate.