Background

On 5 February 2025, the Minister of State for Local Government and English Devolution wrote to all councils in two-tier areas and small neighbouring unitary authorities to formally invite proposals for local government reorganisation (LGR). The government’s intention is that simpler local government structures can lead to better outcomes for residents, improved local accountability and savings which can then be reinvested in public services.

The process of LGR is complex and these Finance Essentials Guides have been developed for Chief Finance Officers, elected members, and LGR programme teams, to aid the development and implementation of local LGR programmes.

They are informed by discussions with a number of councils which have recently been through LGR. They aim to provide practical and realistic advice on key areas where financial issues will need to be considered.

This guidance note focuses on the high-level principles that can be used to develop estimated expenditure, funding and balance sheet positions for the new unitary council/s. This may include both disaggregation of county council (and potentially existing unitary councils’) expenditure, funding and balance sheet positions as well as aggregation of existing district and unitary council’s expenditure, funding and balance sheet positions.

The guide provides advice on how these challenges can be managed covering the key areas of:

- financial modelling to inform budget setting: high level principles

- financial modelling: revenue expenditure

- financial modelling: revenue funding

- financial modelling: balance sheet position.

Context

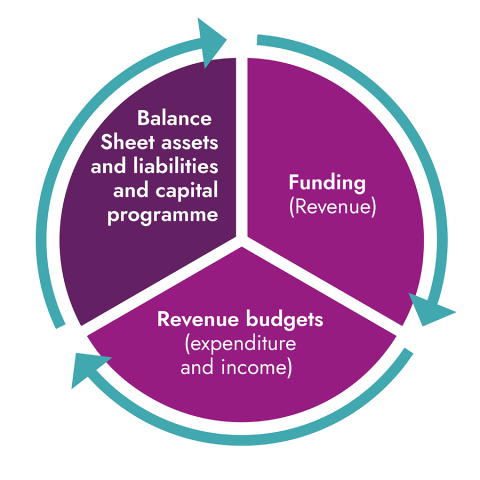

In order to estimate the potential funding, expenditure and balance sheet position of new unitary council/s, complex financial models based on a significant number of principles and assumptions will need to be developed. This is a considerable task, and the amount of time and resource required for this should not be underestimated.

Diagram 1: Funding cycle

Although financial estimates will have been developed to inform the final LGR proposals submitted to government, these will continue to need to be refined and updated as the new unitary council/s are established.

Only once government have confirmed their decision on the creation of new unitary council/s in a particular area can the estimated expenditure, funding and balance sheet positions for these councils begin to be finalised.

The financial models developed for LGR proposals will provide some of the baseline data needed for LGR implementation plans; however, the governance of approving the principles and methods for disaggregation, aggregation and so on will shift from the predecessor councils to the new shadow council/s ahead of vesting day.

Modelling funding and expenditure

Modelling the funding position and of the expenditure position should be done separately. This is because it is unlikely that the funding available will exactly match the spend required to meet demand on services, especially where services are being disaggregated. Understanding these differences is an important step in establishing a realistic budget for year one of the unitary council/s.

Expenditure budgets on specific service areas within the new unitary council/s should be driven by robust data on activity, demand and relevant cost drivers. It is unlikely that funding will exactly mirror patterns of demand and expenditure. Where differences emerge, this will require the shadow council/s to determine how budgets should be reallocated. If expenditure budgets are allocated purely on funding formulae rather than actual demand/spend data, then the new unitary council/s may face significant in-year pressures which require urgent mitigating actions to address.

Shadow council/s are responsible for approving the year one budget for the new unitary council/s and hence will determine their priorities and how the funding will be allocated to reflect this.

Chief Financial Officer/s should obtain assurance on the reasonableness of estimates of demand for services, and the available funding envelope, as part of their reporting on the overall robustness of the budget.

Section 16 Agreements*

Establishing the principles for estimating expenditure, funding and balance sheet positions is an iterative process and will need to be formally agreed by the relevant shadow council/s ahead of vesting day through a formal Section 16 agreement.

This agreement provides the legal process to transfer all of the assets and liabilities (including revenue expenditure) of the predecessor councils to the new unitary council/s. The earlier that principles can be agreed through the shadow council/s the better. Central government will require an implementation plan from the relevant transition body (shadow council/s), which will set out what steps and decisions the body needs to take in order for the new unitary council/s to be ready for vesting day.

Application of the agreed principles within the Section 16 agreement will be externally audited, for example via verification of the opening balance sheet position/s within the new unitary councils’ statement of accounts. A clear working paper and audit trail should be kept in order to demonstrate compliance with the agreed principles.

*Section 16 of the Local Government and Public Involvement Act 2007 (‘Section 16’) and Local Government (Structural Changes) (Transfer of Functions, Property, Rights and Liabilities) Regulations 2008 (‘the Transfer Regulations’)

Financial modelling to inform budget setting: High level principles

During the implementation phase the objective of financial planning shifts to supporting the development of the first annual budget and Medium-Term Financial Plans (MTFPs) for the new unitary council/s. This requires an estimation of the net revenue expenditure positions for the new unitary council/s based on modelled demand requirements and an estimated funding envelope, including assumptions on grant funding, council tax (including assumptions on harmonisation and rate increases), fees and charges income and use of reserves.

Principles for financial modelling must support the relevant statutory financial duties (including the Best Value Duty (Section 26 of the Local Government Act 1999) and professional accounting standards including the CIPFA Code of Practice on Local Authority Accounting.

There is unlikely to be the required capacity or time to do a completely zero-based budgeting approach, so materiality will be a key consideration. Having a de-minimus budget level below which a proxy disaggregation approach is taken can be helpful, for example £1 million or an agreed percentage of the net revenue budget.

Agreeing the level at which budget expenditure disaggregation will take place is also important. Following the CIPFA Service Reporting Code of Practice (SERCoP) descriptions can be helpful as these align with the Revenue Outturn (RO) reporting.

Overall, it will be a combination of materiality, accessibility of evidenced cost driver data and availability of consistent financial budget data that will determine the level of work that budget disaggregation and aggregation will involve.

Other pertinent information will include:

- estimated inflation and pay award assumptions

- estimated Minimum Revenue Provision (MRP) costs and treasury management positions

- estimated opening balance sheet positions

- estimated savings from transformation activities that are proposed to be delivered in the first 3-5 years to deliver on the organisational design and vision ambitions.

Specific issues to consider

Having early discussions on the appetite for shared services across the new unitary council/s (either permanently or on an interim basis) is recommended. Establishing shared services criteria/guidelines can be helpful so that these are agreed in principle ahead of final decisions being taken. If the principle of sharing service/s is agreed, then the shadow council/s will need to decide who will host these and how will they be governed and monitored.

It may not be possible to disaggregate some contracts, for example Private Finance Initiatives (PFI) /Public-Private Partnerships (PPP) so an early decision on which new unitary council will host these and how will they be governed and monitored will be necessary.

Decisions will also need to be taken on hosting the Local Government Pension Scheme (LGPS) which may require one of the new unitary council/s to be established as the ‘administering authority’ for the LGPS, or a separate body to be established.

If there are boundary changes to existing councils then a disaggregation approach will also be relevant to determining the percentage allocation of the expenditure, funding and balance sheet of those areas to the new unitary council/s.

Planning for budgetary decision making

The implementation phase requires a significant number of decisions to be taken by the shadow council/s. As the year one budget and MTFP may be set before a final Section 16 agreement is approved some of the key principles for disaggregation/aggregation will need to be agreed as early as possible once the shadow council is formed.

It is recommended that a forward plan for the shadow council/s is developed as soon as they are established, setting out a clear timeline and overall plan for what decisions are required and when they can be taken. Any decision will need to be agreed by all relevant shadow council/s and hence harmonising this forward plan across the new shadow councils will be essential to enable decisions to be taken in a timely and co-ordinated way.

The LGR programme board should drive decisions through the shadow council/s and ensure sufficient briefing of members across all the affected councils ahead of formal decisions being taken, including detail of the proposals, how these have been identified and why they are recommended.

In some instances, central government may also want to be included in discussions in order to be satisfied that disaggregation/aggregation principles are reasonable and mutual agreement has been reached. Ultimately it will be each shadow council/s CFO and monitoring officer that formally recommend the Section 16 agreement to elected members for approval.

Financial modelling: Revenue expenditure

Budget disaggregation

The principles for disaggregating revenue budgets will be dependent upon the operating models within the existing councils and will require relevant activity and performance data to inform this. It will need to consider the key cost drivers, for example demographics, demand analysis and geographic location of services, and so on. The following are examples of disaggregation principles that could be applied.

- Location service delivered: For example, location of assets - buildings, parks, geographic footprint of service.

- Residence of service user: For example, 'Ordinary residence' principle of social care, where split may be based on home postcode of service user, not location service is delivered.

- Population: For example where costs/ income based upon demand/ usage. May include whole population or sub-set (for example 0-17, 18-64, 65+).

- Other cost/ Income drivers: Underlying drivers for service areas, for example road length, FTEs, number of households, council tax base or business rates tax base, demand data, activity data, performance data.

- Funding formula: Split prescribed within funding terms and conditions, for example Dedicated Schools Grant (DSG), Public Health Grant, Better Care Fund (BCF), Improved Better Care Fund (IBCF) may have specific grant formula/data to allocate the funding. Work ongoing to review formulas where seen as out of date.

- Technical: Disaggregation to follow responsibility, for example corporate costs such as residual pension, teacher additional pension, MRP-specialist advice being provided, depreciation (follow assets split).

For some services activity data may be readily available and can be identified on a geographic basis in order to inform demand predictions and cost estimates for the new unitary council/s. However, for many service areas a proxy measure may need to be agreed to allocate expenditure across the new unitary council/s.

Where detailed data analysis for services is not available it is helpful to agree a default basis for disaggregation across the new unitary council/s. This could be based on either a percentage of total population or percentage of the overall net revenue budget at a fixed date or a percentage net assets position at a fixed balance sheet date.

From a materiality perspective this will provide a simple allocation method that can be refined if and when more detailed activity data is available.

In respect of specialist areas such as the Housing Revenue Account (HRA) and Dedicated Schools Grant (DSG) the statutory requirements for those costs and budgets will need to be adhered to.

Appendix 1 shows possible disaggregation principles for different service expenditure types for county council services. These are suggestions and it will be for each LGR programme and for each shadow council to agree the final approach.

- Step one: Agree which financial year will be the baseline for the budget analysis. For the implementation phase (assuming vesting day is the 1 April 2028) then using the 2027/28 publicly approved budgets may be possible, although to allow early decisions it may be beneficial to use the 2026/27 budget positions.

- Step two: Agree to what level existing budgets will be disaggregated, for example service level/ cost centre level. From a materiality perspective this should not be set too low, but needs to be balanced with the ability to set a robust and deliverable budget in the first year of the new unitary council/s.

- Step three: Apply a disaggregation principle and methodology to the agreed budget lines. For each service area it is recommended that the disaggregation principle should be agreed with the responsible officer for that service area. Where a formal LGR programme has been established it is likely that programme leads for each service area will have agreed and can be involved in approving the application of the relevant principles.

- Step four: Share and agree the proposed principles with elected members. This may involve task and finish groups, the shadow council scrutiny process and shadow council cabinets/ executives. The shadow council decision making window will be short, so approving principles as early as possible is helpful since developing an indicative expenditure position for the new unitary council/s will provide the starting point for the budget setting process.

Service budget aggregation

A Section 16 agreement will also set out the aggregation of any relevant expenditure, funding and balance sheet positions.

In order to aggregate service budgets, financial modelling will need to be explicit about any assumptions on harmonisation of service levels before vesting day and/or require acceptance that there could be differences within a single unitary council footprint on ‘day one’, for example frequency of waste collection, and so on.

Although in theory it should be straight forward to aggregate expenditure budgets across councils, in reality it is likely that services will be delivered differently across the predecessor councils. Sharing budgetary information early in the process so that the detail can be understood and mapped will help to establish a robust year one budget for the new unitary council/s.

From a service delivery perspective, the shadow council may want to determine how services will be delivered in the first year; however these will continue to be delivered by the sovereign councils up until vesting day, so any ability to reshape or change service provision is limited in the short-term. An LGR programme will help to manage this and establish any quick wins in respect of harmonisation after vesting day.

Financial modelling: Revenue funding

The principles for disaggregating / aggregating revenue funding streams will need to be determined and agreed by the shadow council/s ahead of vesting day.

Pending further guidance from government on agreeing local funding splits, potential approaches that can be adopted are set out in more detail below.

Central government general grants

Principle: General grant allocations for the new unitary council/s can be estimated on the basis of the underlying data used to determine the different elements of the national funding formulae.

The latest local government finance settlement data can be used to model potential funding envelopes for the new unitary council/s. Ultimately it will be the provisional finance settlement 2028/29 that will determine the central government funding available to the new unitary council/s.

In recognition that local government reorganisation will change the structure of local authorities the government will set a ‘funding envelope’ for the new local authorities created where areas reorganise. This envelope will be set by combining the grant allocations of the relevant local authorities in the year(s) of the multi-year settlement following reorganisation. To provide certainty, government will not recalculate allocations, including any funding floor payments, based on new unitary geographies in this multi-year settlement period.

It will be for local areas to agree how to divide the funding where the establishment of new unitary authorities means existing local authorities are split. The government will provide guidance to local authorities on how to arrive at local agreements and will set out a timeline for when these agreements must be reached. The government recognises the competing pressures of local areas needing to agree the funding split as soon as possible ahead of vesting day for the new authorities, as well as the need for government to review the agreement and incorporate it through the usual settlement process. If areas are unable to reach an agreement, the MHCLG Secretary of State will make a determination on the share of settlement allocations due to new unitaries. The government is clear that the use of a backstop is a last resort and areas should make every effort to come to local agreement. An indicative timetable is set out below.

Indicative timetable

Table 1: Indicative timetable for local government reorganisation

| Milestone | Surrey | All other areas |

|---|---|---|

| Elections to new authorities | May 2026 | May 2027 |

| Area-led final agreement on division of funding | Summer 2026 | Summer 2027 |

| First incorporation of funding division into provisional LGFS | December 2026 | December 2027 |

| First incorporation of funding into final LGFS | February 2027 | February 2028 |

| New authorities vesting day | April 2027 | April 2028 |

Case study: Cumbria

During the local government reorganisation in Cumbria, national funding formulae were used as the basis to model potential funding allocations, updated for latest information on population, activity data, and so on. These were agreed by the two shadow councils and with government. Apart from Public Health, the national formulae were adopted with no technical amendments. An agreement on an appropriate funding formula for Public Health was agreed at the time with the Director of Public Health and MHCLG. Once the updated funding formulae had been agreed this was shared with MHCLG and utilised for the draft local government finance settlement announcement in December 2023. The overarching principle was that the overall grant funding envelope for the existing Cumbrian footprint had to remain the same with funding allocated across the two new unitary councils through financial modelling and joint agreement.

Specific grants

Principle: Grants should be allocated to match the specific service areas they are funding.

For modelling purposes, it will be necessary to understand which grants are being are treated as specific service grants (included within net budget calculations) and which grants are treated as ‘general grants’ (support the funding of the net budget position).

Where specific grants are required to be disaggregated it may be possible to do this using the original formula allocation basis if available.

Council Tax

The Local Government (Structural Changes) (Finance) Regulations 2008 places specific requirements and methodology of calculation onto councils with regards to the calculation of council tax and its harmonisation across successor councils. It is a complex area and for modelling purposes clear assumptions will need to be identified for budget setting purposes.

The Council Tax Base allocation should be straightforward and will be determined according to the billing authorities’ council tax base, i.e. on a geographical basis. The tax base will include assumptions around collection rates and although this may not be materially different across the existing sovereign councils it will be important to document any assumptions on future collection rates as part of the financial modelling process.

Harmonisation of Council Tax

The Local Government Finance Act 1992 requires local authorities to set a single basic level of council tax for their area (the Band D equivalent charge). Therefore, new unitary council/s will require a single rate to be calculated across their area. This could result in significant changes to some bills and/or a significant change of income for the new council/s; therefore, statue allows the new council/s to harmonise over a maximum of 7 years. A uniform level of council tax must be in place by year 8 of the new council/s.

Harmonising council tax rates at the weighted average Band D rate means that the overall yield for the area will be maintained. This has been the preferred approach for many new unitary council/s especially where harmonisation has been agreed from day one.

The referendum principles for limiting excessive increases still apply but they can be applied to the predecessor areas or to the overall weighted average Band D charge. Some new unitary council/s have managed the gradual harmonisation process by applying the referendum threshold to the predecessor areas’ Band D rates rather than the weighted average Band D rate.

The decision on Council Tax harmonisation is for the new shadow council/s to take balancing three key factors:

- Resources: maximising resources available to the new councils to ensure greatest level of financial sustainability.

- Equity: Ensuring everyone in each new council area pays the same.

- Political priorities: For example, not increasing by the maximum allowed to account for local cost of living pressures.

Understanding the size of the gap and hence the potential impact on council taxpayers is important. This can be a significant political risk and have a material financial impact if harmonisation is planned over a number of years. This may reduce the overall council tax income for the new unitary council/s in those early years.

The assumptions within the financial model must state what the approach is and be consistently applied.

Similarly, council tax policies for second home premiums, empty homes premiums and discretionary reliefs should be documented. It will be a decision for the new shadow council/s as to whether harmonisation of policies will happen for vesting day or not. For some areas this may not be financially material but for others, for example where there is a significant empty home premium this could be material.

Council Tax Reduction Schemes (CTRS)

Councils have discretion to set their CTRS locally and it is likely that different schemes will be in place across the new unitary council geographies. This is a complex area, so for modelling purposes clear assumptions should be documented and applied consistently. The political aspects of harmonising CTRS should also be considered, since this policy will have a direct impact on those council taxpayers least able to pay.

Systems considerations

It is important to establish whether existing revenues and benefits systems will continue to be used by the new unitary council/s initially or whether a single system can be established prior to vesting day. If existing systems are maintained they will need to be capable of producing a consistent council tax bill across the whole geographical area of the new unitary council. Any change to revenues and benefits systems can be complex and this is an area where the shadow council/s will need to consider whether investment in systems change pre vesting day is required and can be realistically implemented in within the required timeframe. Overall, the priority should be to ensure that the new unitary council can consistently apply their agreed revenues and benefits policies on vesting day.

Business rates

The Settlement Funding Assessment (SFA) is an individual local authority’s share of total local government funding settlement. It is currently comprised of the authority’s Revenue Support Grant allocation and its Baseline Funding Level (BFL). The BFL is effectively the share of business rates funding that government determines an individual local authority needs to deliver local services.

Where existing individual councils are aggregating for the purposes of LGR then modelling the new BFL is relatively straightforward. However, where a council will need to be disaggregated then a methodology to split the BFL is required. Historically this has been down to the new unitary council/s to determine and has been based either on a single distribution factor or individual components within the SFA split on different factors. For financial modelling purposes it will need to be determined which approach will be assumed and how this has been calculated.

As part of the implementation phase agreement on this will need to be taken by the shadow councils and agreed with MHCLG in order to inform the local government finance settlement figures for the new unitary councils (see Central Government General Grants section above). MHCLG may determine which approach they wish to use for all new unitary councils.

Fees and charges

Principle: Income should be allocated to the services to which the fees and charges relate, as this will form part of their gross budget position.

Fees and charges are likely to be a material source of income for councils, particularly those with Adult Social Care responsibilities. It is critical that there is consistency in the approach being taken to disaggregate/ aggregate social care costs with the disaggregation/ aggregation of personal contributions. For modelling purposes income could be apportioned according to the split of spend in specific service areas, for example home care, residential care.

Decisions around harmonisation of fees and charges will be required as part of establishing the new unitary council/s. This is a potential area for additional income generation if the base assumption is that fees will be increased to the highest existing charge.

It is recommended that detailed analysis of the different fees and charges of the predecessor councils is undertaken early in the implementation programme, with modelling undertaken to establish what a harmonised ‘fee’ or ‘charge’ could be for the new unitary council/s. Fees and charges can be politically sensitive and so early discussion on how and when harmonisation of charging (for example, green waste) and of charging levels (for example, parking fees) should be planned into the programme. It may not be feasible to harmonise all fees and charges on day one but a clear statement on the expected timeline to do that should be stated within the fees and charges policy for the new unitary council/s.

Financial modelling: Balance sheet position

The principles for disaggregating and aggregating balance sheet positions will need to be determined and agreed by the shadow council/s. Potential approaches that can be adopted are set out in more detail below.

The actual balance sheet position for the new unitary council/s will only be determined once the final closing balance sheet positions for the existing councils for the financial year prior to vesting day are published and audited.

Overarching principles for allocating/apportioning balance sheet items

Fixed assets such as buildings and equipment

Principle (disaggregation and transfer): For those assets with a fixed location such as land and buildings it is likely to be assumed that these will transfer on a geographical basis linked to the proposed service delivery models and to support the overall organisational design for each new unitary council/s.

- For operational assets the overarching principle is likely to be that they transfer on a geographical basis.

- For assets under construction the overarching principle is likely to be that they will transfer on a geographical basis linked to the service delivery models they support.

- For investment assets the overarching principle is likely to be that they will transfer based on a geographical basis, ensuring that the associated income streams are incorporated into the funding envelope for that authority.

- For assets held for sale as at vesting day is likely that these will transfer based on a geographical basis or that the proceeds of the sale will be apportioned to the new unitary councils using an agreed split.

- For PFI/PPP assets that are fixed in location is likely that these will transfer based on a geographical basis linked to the proposed service delivery models with both balance sheet and revenue streams transferring.

- For vehicle, plant, furniture and equipment and intangible assets it may be assumed that these will transfer on a geographical basis if this can be identified or otherwise agreement should be sought to split on an equitable basis to support the proposed service delivery models.

Further guidance on understanding the implications of how assets are allocated to the new unitary council/s will be published as a separate note.

Local authority owned companies

Where these fall neatly within the boundaries of the proposed new geographies then these should transfer to the relevant unitary council/s. If they need to be disaggregated, then a decision on future ownership of the company will need to be taken and this will then determine the allocation of the related income stream and asset/ liabilities.

Also note that shareholder agreements and articles of association may need to be updated as part of the LGR implementation work.

Long term borrowing

Principle: the council/s’ borrowing requirements are managed as a whole in order to fund the capital programme and therefore individual loans are not allocated against individual assets.

From a debt repayment perspective each predecessor council will have their own Minimum Revenue Provision (MRP) policy which determines the value of debt that is accounted for each year, resulting in a capital finance requirement (CFR).

For the new unitary councils their MRP policy will be set as part of the Treasury Management strategy agreed by the shadow council/s as part of the budget setting process leading up to vesting day.

The overarching principle for the disaggregation of the associated CFR and actual debt (long term borrowing) should be to ensure that the appropriate allocation of the CFR and associated MRP against relevant assets is maintained. This is then linked to the appropriate level of external borrowing identified and a fair split of the debt in respect of maturity dates interest rates, and so on.

This is likely to require disaggregation of upper tier councils’ asset values and aggregation of lower tier councils’ asset values. The approach will ensure that the CFR created for each new unitary council/s will fairly reflect the assets transferred.

The net book value of any disaggregated assets will be adjusted to exclude assets that have not previously been financed by borrowing where this information is available.

For pre 2008 supported borrowing there is unlikely to be sufficient information to identify which assets were funded from the borrowing therefore a proxy disaggregation method will be required. An example could be the net book value of land and buildings on the balance sheet to be disaggregated split by geography.

For prudential borrowing an approach could be to identify the estimated value of assets to be disaggregated to each new council that have either already been financed from borrowing or will need to be financed from borrowing. The proportion that this sum represents for each authority will be used as the percentage to split the remaining capital financing balances. Given the sensitivity and complexity of allocating debt to new unitary councils from existing capital portfolios it may be necessary to require specific technical advice in this area with potentially arbitration and/or discussions with government on the approach to be taken where extreme levels of debt are identified.

Where there are PFI/PPP schemes these should be identified separately within the CFR and can be allocated directly to the appropriate new council. If the PFI/PPP is delivered across a number of new unitary councils, then a single unitary will host the contract and relevant CFR and appropriate recharges will need to be established as part of the shared contract arrangements.

This approach has been used by a number of unitary councils including the disaggregation of Cheshire County Council into Cheshire West and Chester and Cheshire East councils. Once the CFR has been disaggregated it is for the new shadow council/s to approve their own MRP policies and apply those within their financial statements.

This is a technical and potentially contentious area so early work to gather data and understand the options available is recommended.

Current assets: Inventories

Principle: Inventories should be allocated based on geographical location and/ or service delivery models.

Current assets: Debtors and payments in advance

Principle: All debtors should transfer aligned to the service area that they relate to (including deferred charges on client property in respect of social care charges). Any transfers of debt should be matched with the relevant bad debt provisions set aside under the provisions in the balance sheet. For modelling purposes, a proxy split based on overall percentage net revenue budget for each new unitary / population percentage could be used.

Current assets: Cash and cash equivalents

Principle: All cash and cash equivalents should be allocated to match reserves, provisions and net debtor and creditor balances. Where cash balances support internal borrowing positions they will be allocated as part of the overall external borrowing/ debt allocations.

Contingent assets

Principle: Contingent assets should be allocated based on the associated agreements/assets/risks/schemes/service areas that they relate to.

Current liabilities

Principle: debt (external or internal) should be allocated based on the assets to which the debt relates either in totality or as a percentage of assets and debt. This includes short term borrowings.

Creditors and receipts in advance

Principle: All creditors should transfer aligned to the service area/activity that they relate to. This includes receipts in advance and grants. For modelling purposes, a proxy split based on overall percentage net revenue budget for each new unitary / population percentage could be used.

The creditor associated with accumulated absences can be matched against the entry under the Accumulated Absence Account Reserve (AAAR). In the interest of completeness in agreeing the opening balances of the new unitary council/s the balance on the AAAR could be apportioned based on the proportion of employees transferring to the unitary council/s.

Provisions

Principle: All miscellaneous provisions will be allocated based on the specific cases, matters and/or individuals to which they relate.

General Fund Reserves

Principle: The overarching principle is that the reserves should align with the relevant risks for which they were identified and allocated on that basis. For general fund reserves aggregation of lower tier authority reserves is likely to be required, and disaggregation of upper tier authority reserves. In Cumbria this was based on the net revenue budget position percentage for each new unitary (based on an agreed version of the financial modelling for both funding and expenditure).

Earmarked revenue reserves (non-DSG)

Principle: specific reserves are allocated based upon the originally intended purpose and will be aligned with the asset or risk for which they are required. For example, a PFI reserve would be allocated to the new unitary council where the PFI asset is transferred.

Where there is no clear allocation methodology linked to risk and activity then it is proposed that a population based percentage approach will be taken.

Capital earmarked reserves

In respect of unused capital receipts and usable capital financing reserves these can be allocated based on the principles adopted for asset allocation above and where appropriate proportionately used to reduce debt.

DSG reserves

Where these relate to balances of specific schools then these should be allocated based on the geographical location of the schools within the new unitary area/s. For non-school specific DSG reserves please refer to the separate DSG guidance note that will provide the relevant advice.

Technical accounting adjustment reserves

Principle: These reserves should be disaggregated in accordance with accounting requirements.

Summary

Across all financial modelling the consistency and quality of data sets used is important. Clearly documenting any assumptions made and any local agreement on the approach used is also critical.

Shadow council/s can refer to the financial modelling used in the final proposals but ultimately will need to agree any assumptions used to determine the budget for the new unitary council/s as part of the implementation phase. Some of these may need to be agreed with other unitary council/s across the new geographies being established and, in some instances, may require a level of independent arbitration if local agreement cannot be reached in the first instance.

One of the key drivers of LGR is to establish financially sustainable unitary councils who are resilient enough to respond to financial risks. This requires the new unitary council/s to have a year one budget and MTFP that is built on reasonable estimates and demonstrates that the estimated spend for the year can be fully funded. The greater the level of understanding on how expenditure budgets have been established and how the funding has been allocated, the greater the likelihood that the budget can support service delivery effectively.

Once the initial budget disaggregation/aggregation work is completed and agreed it will be for the shadow council/s to decide how to allocate the overall expenditure budget to achieve delivery of the new council corporate plan and priorities within the financial envelope available.

Appendix 1: Example disaggregation principles

Table 2: Example disaggregation principles: Corporate services

| Corporate services | Potential disaggregation method |

|---|---|

| Communications | Population |

| ICT |

Activity data No of staff Types of users Data usage |

| HR, payroll and OD | Staff numbers |

| Health and safety | Staff numbers |

| Trade Union facility time | Staff numbers |

| Library services | Geography location |

| School Library services | Geography -School pupil numbers |

| Legal services | Case load |

| Democratic services and political support | Councillor numbers |

| Scrutiny officers | Councillor numbers |

| Member allowances | Councillor numbers |

| Commissioning (staffing) | Commissioning spend % |

| Procurement | Contract spend |

| Archives | Population |

| Residual Pension Costs | Population |

| Coroners | Population |

| Registrars | Population |

| Finance and Internal audit | Net Revenue Budget |

|

Fleet (Home to school transport should be reviewed separately) |

Geography No of staff for pool cars, and so on. |

| Assets management and property (Corporate landlord) | Geography of assets |

| Insurance |

Modelled by actuary Staff then split on usage |

Table 3: Example disaggregation principles: Place services

| Place Services | Disaggregation method |

|---|---|

| Community / area support | 50/50 or population split for ‘operational’ areas |

| Highways -operational teams | Highways funding formula |

| Winter maintenance | Road mileage within winter maintenance programme spit on geography |

| Parking enforcement | Geography |

| Economic development |

Population Geography |

| ENCTS | Over 65 population |

| Street lighting | Geography |

| Street works | Road mileage by geography |

| Trading standards | Population |

| Waste disposal | Tonnage |

| Development control and regulation | Population |

| Depots | Geography |

| Salt | Road mileage within winter maintenance programme spit on geography |

Table 4: Example disaggregation principles: Children's services

| Children’s Services | Disaggregation method |

|---|---|

| Home to school transport | Registered address of pupils |

| Virtual school | No of Looked After Children |

| Learning improvement service | No of schools |

| Admissions team | No of schools |

| Education Psychology | Activity data |

| Children and families management and support |

Geography if already established in locality teams Activity data |

| Fostering team | Residence of foster carer |

| Fostering allowances | Actual data linked to child |

| Children’s residential homes | Geography |

| Carers and short breaks | Geography |

| CLA commissioned costs | No of Looked After Children |

| Youth offending team | Population 0-19 |

| Early help | Population 0-16 |

| DSG | See separate guidance note |

| Outdoor centres | Geography |

Table 5: Example disaggregation principles: Adult services

| Adult Services | Disaggregation method |

|---|---|

| Social Care – staffing |

Geography if already established in locality teams Activity data |

| Carers support | Population >65 |

| Community Finance | Population >65 |

| Nursing / Residential provision – older adults ( >65) |

In house provision – geography Commissioned – ordinary residence |

| Shared lives | Service user geography |

| Supported living – older adults (>65) |

In house – geography Commissioned – ordinary residence |

| Supported living – working age adults (18-64) |

In house – geography Commissioned – ordinary residence |

| Reablement | Population >65 |

| Safeguarding adults board | May require additional disaggregation costs |

| Client affairs | Population >65 |

| Public Health | Activity data/ Funding formula |